Table of Contents

- Introduction: Why Mortgage Support Matters for Expats in Germany

- Mortgage Broker Germany vs Mortgage Advisor Germany

- When to Use a Mortgage Broker in Germany as an Expat

- Mortgage Calculator Germany: Useful First Step, But Not Approval

- Mortgage Rates Germany: Why the Lowest Rate Is Not Always the Best Mortgage

- Home Loan Germany: How the Mortgage Process Works

- What German Banks Check Before Approving a Mortgage

- Mortgage Broker Germany Costs: How Brokers and Advisors Get Paid

- Mortgage Broker vs Bank Germany: Which Is Better for Expats?

- Common Mortgage Mistakes Expats Make in Germany

- How Finance for Expats Can Help With Home Loan Support

- Frequently Asked Questions About Mortgage Broker Germany

- Final Thoughts: Finding the Right Mortgage Support in Germany for Your Home Loan Approval

Germany can be a bit of a minefield for mortgage financing for international buyers, as there is a lot of paperwork and many requirements from banks. Not all banks are flexible enough for foreigners, and expats often need a helping hand with mortgage financing for a property purchase in Germany. Therefore, this article gives a few hints and tips on mortgage financing for property in Germany as an international buyer.

In this article, we describe the home loan support services provided by mortgage brokers in Germany, independent mortgage advisors in Germany and banks in Germany. We explain how mortgage calculators function. We present an overview of mortgage rates in Germany. We describe in detail the approval requirements of German mortgage lenders. We explain which documents are required by banks for mortgage approval. The search for the best home loan in Germany is not limited to finding the lowest interest rate. The goal is to find the most suitable home loan in Germany, with strong approval chances and suitable terms and conditions for each individual client.

Introduction: Why Mortgage Support Matters for Expats in Germany

As an expat, it is often more difficult to obtain a mortgage in Germany than it is for a German citizen. In order to grant approval for a mortgage, German banks check a variety of different criteria. These include the stability of your income, the amount of equity you have, your "SCHUFA" credit rating, your residence status and the documents for your property. Many of these factors can be problematic for expats, especially if they have recently moved to Germany, earn their income abroad or are self-employed.

Finding home loan support for buying property in Germany as an expat can be very difficult indeed. Because of a number of additional factors a German bank will use to assess your mortgage application, things can be much more complicated than for homebuyers with permanent German residence. As with anything in life, the biggest single mistake most expats make when considering a German mortgage is searching for the perfect German property for sale first and then trying to sort out a mortgage later on. Agents and sellers are very used to expecting potential buyers to first establish clearly that they have financing in place for their chosen German property. It can be extremely frustrating and a complete waste of time for expats if banks take two or three weeks to formally decline a mortgage application.

Mortgage Broker Germany vs Mortgage Advisor Germany

A mortgage broker and a mortgage advisor are terms that are often used equally in Germany and are also often mixed up by foreign property buyers looking for the right type of financing for a property. The difference between the two terms is simply that the term mortgage broker is more commonly used, whereas the term mortgage advisor explains better the tasks that a mortgage advisor fulfills when searching for the right mortgage for a buyer.

First of all, a mortgage advisor explains the different types of mortgages offered by the banks to the client and in detail. He will explain what the structure of a mortgage is, what the repayment of a mortgage means for a buyer, and last but not least what the risks are for a buyer when repaying a mortgage. In summary, an independent mortgage advisor will explain all of the structures of different types of mortgages to his clients, including the affordability of a mortgage for each buyer individually and the potential risks that each different type of mortgage offers the buyer.

For expats, the first question to ask is whether they fit the usual profile of a German mortgage borrower. As a single bank can only offer the mortgage products of its own bank, a mortgage broker in Germany can compare the mortgage offers of many German banks with each other. On this basis, the mortgage broker can determine which bank may grant a mortgage for which applicant.

What a Mortgage Broker in Germany Does

A mortgage broker Germany will not only compare the interest rates of the various home loan products, but also the terms of repayment of the various home loans for foreigners in Germany. A mortgage broker can also establish which lender will most likely approve a home loan for a foreigner.

A foreigner who is searching for a home loan in Germany will often be better off with a mortgage broker than with only one bank. The mortgage broker will also prepare the financial documents for the home loan application and submit these to suitable home loan lenders. If one of the home loan providers declines a home loan application by a foreigner, this can be frustrating and may also affect the broader application process. Therefore, it will be in the best interest of many foreigners searching for a home loan in Germany to have their application processed strategically by a mortgage broker for various home loan providers in Germany. The foreigner can then compare the various home loan products and also know that the application has been placed with more suitable lenders.

What a Mortgage Advisor Germany Does

An independent mortgage advisor offers independent mortgage advice to expats and specializes in the financial planning of a mortgage. An independent mortgage advisor assists expats in choosing the correct mortgage product from a range of financial products available on the market.

An independent mortgage advisor in Germany can check whether a proposed mortgage offer is affordable for the expat in terms of the repayment schedule and the potential effect of the mortgage on the expat's other finances. By assisting expats in this way, an independent mortgage advisor can help expats avoid making very costly mistakes with their mortgage in Germany.

When Going Directly to a Bank Can Work

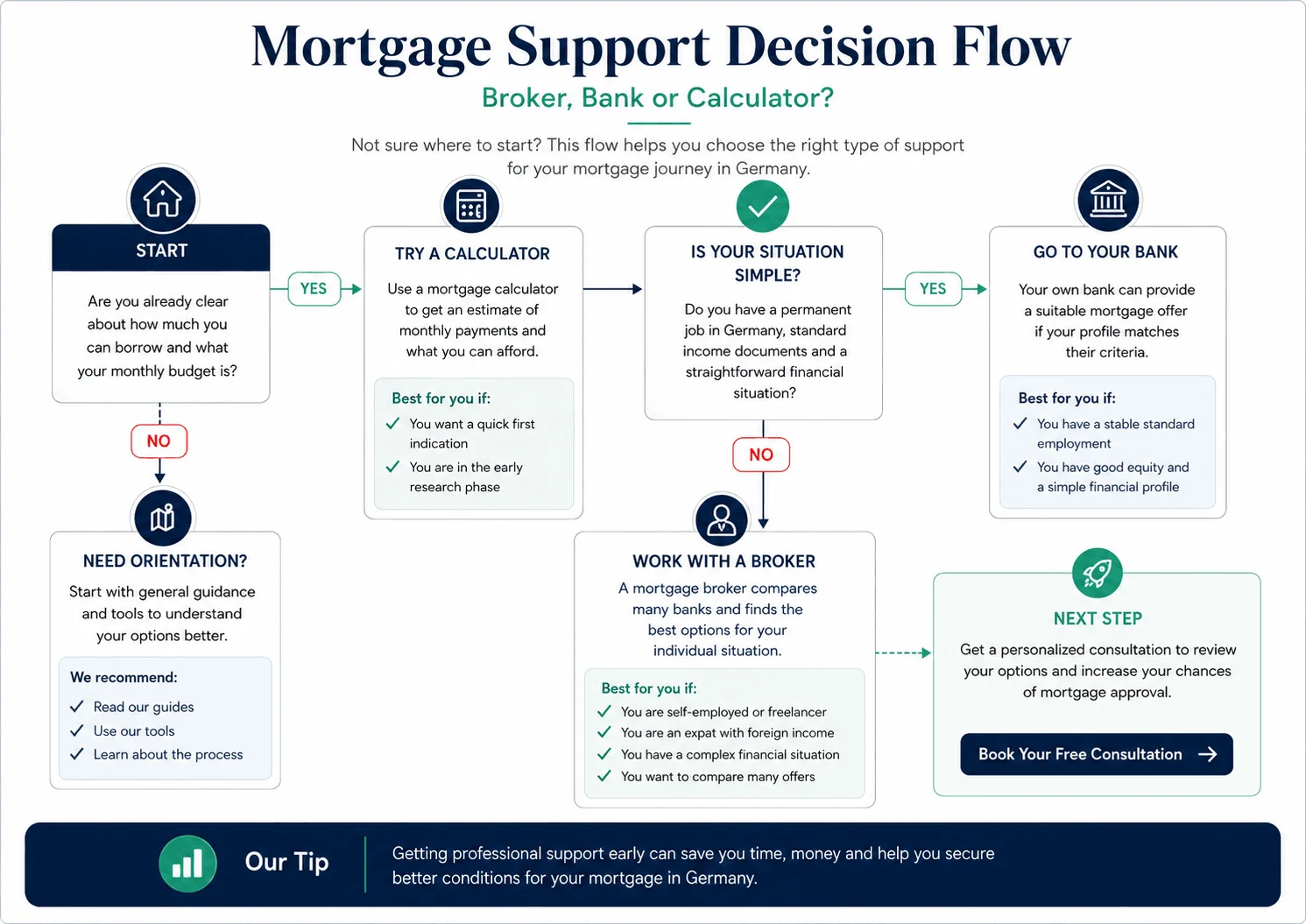

It is generally very efficient and no problem for expats with permanent German employment and a lot of equity to get a mortgage directly from a bank. Existing customers of a bank may also receive favorable terms. However, as soon as the customer profile is a bit more complicated, the bank has less room for maneuver.

When to Use a Mortgage Broker in Germany as an Expat

Even simple mortgage agreements are usually organized between the buyer and the bank itself in full and without complications. However, in more complex cases, with foreign income or self-employment income, a mortgage broker is often better suited than going to only one bank.

You Have Foreign Income or Recently Moved to Germany

Foreign income complications can be difficult for foreign borrowers when looking for a mortgage in Germany. A lot of banks are unfamiliar with foreign tax situations and foreign language income contracts. That is why an experienced mortgage broker in Germany for expat mortgage solutions can be so important. He can present the situation of the foreign borrower in the best possible light to lenders that are used to dealing with mortgage for foreigners cases.

You Are Self-Employed or a Freelancer

Loans for self-employed individuals in Germany can be more challenging for banks to approve than loans for salaried employees. To grant approval for a loan for self-employed individuals, the bank requires tax assessments and profit and loss statements for a minimum period of two years, to verify the applicant’s stable income. A broker that specializes in expat mortgage cases for self-employed buyers can help match you with the right German bank and increase the likelihood of mortgage approval in Germany.

You Need Mortgage Approval Germany Quickly

Whether you need to present it to real estate agents or to potential sellers, it is very valuable to have a "Finanzierungsbestätigung" (Financing Confirmation) with you. A mortgage broker or mortgage advisor can help prepare a financing confirmation that states your financial position would most likely receive approval for a mortgage. This does not mean that final approval for a loan has been granted, but as a buyer you are provided with a powerful tool.

For more detail on this topic, you can also read our guide on mortgage approval and financing options for expats buying property in Germany.

Mortgage Calculator Germany: Useful First Step, But Not Approval

A mortgage calculator can serve as a home loan calculator and an investment calculator. A property loan calculator helps you work out how much home loan you can afford. Similar tools can help give you a first idea of repayment before contacting a financial advisor or bank. However, no online mortgage application can serve as mortgage approval and should not be used in place of proper advice or as a substitute for applying for finance.

What a Mortgage Calculator Germany Can Show You

It shows estimated monthly repayments as well as the other implications that buying a home has for your cash flow. Additionally, there are property investment calculators. These can help you work out if the return on investment for a property will be sufficient for you.

If you want to test monthly cash flow, acquisition costs and long-term return assumptions, you can use the Property Investment Calculator as a practical starting point.

What a Mortgage Calculator Cannot Tell You

As mentioned before, no online mortgage calculator has any information about the individual circumstances of a person. No online mortgage calculator has access to the "SCHUFA" credit information of a person, whether or not the person is resident in Germany, whether the person is employed or self-employed, on what income they are basing their mortgage application, and what documentation they have in place to prove their residence in Germany.

In addition, a mortgage calculator does not know whether the proposed property for a mortgage will actually be accepted in a valuation by a bank. The mortgage calculator will have calculated the mortgage payments on the basis that the property is accepted in a valuation by the bank and that the borrower has provided all the required documentation for a mortgage application. Unfortunately, this is not always the case.

Mortgage Rates Germany: Why the Lowest Rate Is Not Always the Best Mortgage

This is certainly a hot topic in the German mortgage market. Many interested buyers start their search for home finance by comparing home loans on the basis of their interest rates. Lowest interest rate first. However, there are some very important other factors that can influence your mortgage interest rate. In this section, we explain why a low interest rate on a home loan is not the only important factor in your home search.

What Influences Mortgage Rates in Germany

The interest rate on a home loan in Germany is influenced by a variety of parameters, including the amount of equity a borrower has in relation to the loan amount, the "loan to value" ratio, the fixed interest period, the "Sollzinsbindung", the repayment rate and other aspects, including the borrower’s income. Importantly, the interest rate published by mortgage providers for home loans in Germany is not necessarily the rate that a borrower will be charged. When applying for a mortgage, the bank will draw up a completely individual offer for the borrower.

Fixed Rate Mortgage Germany and "Sollzinsbindung"

Many expats are interested to know that for home loans in Germany it is common practice to agree fixed interest periods, also known as "Sollzinsbindung". Typically, the "Sollzinsbindung" is set for a fixed period of 10 years, however some home loans in Germany can be set for a period of 15 or 20 years.

It is very important to understand that if you agree a fixed interest period for your home loan, then your monthly repayments will remain the same for the agreed fixed interest period, even if market interest rates have fallen. This type of mortgage is secure for expats that have settled in Germany and are looking to buy a property. However, there can be penalties for early redemption of the fixed rate mortgage. As with any financial product, it is crucial that you fully understand the agreed terms prior to signing any contracts.

Variable Rate Mortgage Germany

A variable rate mortgage Germany is granted to buyers as well. Variable rate mortgages are, however, due to high interest risk less popular. A variable rate mortgage can be suitable for a buyer who expects to sell the property in a few years. A buyer may also take on a variable rate mortgage when expecting interest rates to decline. The vast majority of buyers, however, are long-term buyers and therefore choose a fixed rate mortgage.

Home Loan Germany: How the Mortgage Process Works

Furthermore, we have also outlined the mortgage process for home loans in greater detail to ensure you are fully informed throughout the home loan process in Germany and can avoid costly delays along the way.

Step 1: Budget and Affordability Check

To determine your real estate budget for buying houses and apartments in Germany, your mortgage affordability calculation for home loans also has to include the various purchase costs when buying a house or apartment in Germany. These include notary costs, the costs to be registered at the land register, the "Grunderwerbsteuer" and other costs to be paid when buying real estate.

These home buying costs often have to be covered by your savings and are therefore not always included in your mortgage financing. Using an online mortgage calculator at the beginning will give you a first rough estimate of your housing budget. Experts of various banks and lenders for mortgage financing will later check your calculations in detail.

Step 2: Mortgage Documents Germany

German banks for home loans demand a large amount of documentation. This can change from bank to bank and even from case to case at the same bank. But here is an overview of typical papers required by most German mortgage lenders: recent payslips, copies of employment contracts, several months of bank account statements, income tax returns if the borrower is self-employed, residence permits for foreign nationals, credit reports or "SCHUFA", proof of own equity, and documents for the property to be financed, such as the land register extract.

Step 3: Mortgage Comparison Germany

Compare not only the interest rate for a fixed term for a mortgage, but also the term, the initial repayment percentage, the overpayment options of a mortgage and last but not least the lender’s experience with similar types of borrowers. Do not be deceived by low interest rate terms initially for home finance, as they could prove to be more expensive after some years.

Step 4: Mortgage Approval Germany and Financing Certificate

A so-called pre-approval for a mortgage in Germany, the "Finanzierungsbestätigung", is usually sufficient for a seller and a real estate agent to consider a potential buyer seriously. Final mortgage approval in Germany is only granted by a bank after they have viewed the house to be purchased, a valuation has been carried out and the bank has made a full credit assessment.

What German Banks Check Before Approving a Mortgage

Income Stability

Mortgage banks look for borrowers with stable and secure income. Most banks require employment contracts with permanent positions and ask for recent pay slips. During the probation period, called "Probezeit", the banks are more cautious and classify applicants with temporary contracts as higher risk borrowers.

Bonus payments are also discounted and considered when assessing an applicant’s income and creditworthiness. Freelancers and self-employed individuals, as well as those who earn foreign income, are also considered higher risk borrowers and may be asked for additional documentation to support their application. The most important factor is whether the borrower will be able to repay the loan over the course of the mortgage term.

Equity and Loan to Value Germany

The amount of equity required when financing a property forms an important risk metric for the lender. In general, the higher the amount of equity, the better the interest rate for the home loan will be and the more likely the approval of the mortgage application becomes. The amount of equity required often corresponds to around 20 to 30 percent of the purchase price plus the costs of the purchase. This type of financing is also linked to "Eigenkapital Baufinanzierung".

SCHUFA Mortgage Germany and Credit History

Note also that a thin credit file can hinder a mortgage application even if you have a good credit score. Even though your "SCHUFA" credit score might be sufficient for a mortgage, "SCHUFA" history is an important component in the lender’s decision. A well-structured search for your mortgage and a methodical, well-organized application process can help to protect your credit file from potential damage.

For more background, you can read our guide on SCHUFA for foreigners and why it matters for property buyers.

Mortgage Broker Germany Costs: How Brokers and Advisors Get Paid for a Mortgage in Germany

In Germany, the mortgage broker is usually paid by the lender for setting up a mortgage. In most cases, the fees are included in the interest rate of the mortgage, so there is no additional charge for using a mortgage broker. Some independent mortgage advisors may charge a fee for their services. Other mortgage advisors Germany are paid by a combination of the lender’s commission and a fee from the borrower.

It is therefore very important to ask your mortgage advisor how they are being paid before going ahead with a mortgage application. Mortgage advice from a "free" mortgage broker Germany can be of a high standard, however it is always better to check.

Questions to Ask a Mortgage Broker Germany

Before you decide to go to a mortgage broker for searching for mortgage offers on your behalf, it is wise to first ask the following questions:

- How many banks will the mortgage advisor compare for the mortgage?

- Do you work with expats? How many expats have you helped?

- I have foreign income, will the mortgage advisor be able to assist me with my finance in Germany?

- I am self-employed, will I have problems with the mortgage application in Germany?

- How is the mortgage advisor Germany paid for his work?

- Will the mortgage advisor also be able to assist me in preparing the necessary papers for the bank?

- Will the mortgage advisor also be able to compare written offers from all the banks that he has searched for me?

- Will the mortgage advisor be able to explain the structure and risks of the mortgage offer, and not only compare the interest rates of the mortgage offers?

This will give you an idea of whether your mortgage advisor Germany is working for you or if he is simply processing your application through his system.

Mortgage Broker vs Bank Germany: Which Is Better for Expats?

When a Bank Mortgage in Germany Can Be Enough

A simple case would be, for example, a German resident earning German income with sufficient equity in the property and a clean "SCHUFA" credit report. Such a customer can obtain a mortgage at a bank quickly and efficiently as a retail customer. Large German banks have competitive mortgage products on offer for such cases.

When Mortgage Brokers Are Usually Better

Mortgage advisors, however, offer huge value to applicants for home loans who are expat mortgage applicants. If you are an expat and require a mortgage or home loan for a German property, then you need a mortgage advisor or mortgage broker with considerable experience of not only German mortgages, but also mortgages for expats.

Common Mortgage Mistakes Expats Make in Germany

- Searching for property before checking financing.

- Using a mortgage calculator and assuming this equals approval.

- Comparing interest rates for mortgages without checking if you would be approved for the loan.

- Ignoring the purchase costs that are not covered by the loan.

- Applying to several banks without a strategy and risking unnecessary friction with your "SCHUFA" profile.

- Not preparing all necessary documents in good time.

- Not asking enough questions about "Sollzinsbindung", repayment and what happens when the fixed interest period ends.

How Finance for Expats Can Help With Home Loan Support for a Home in Germany

Mortgage advisors can help expats in Germany who are searching for home loans in Germany. They can give expats advice on finance options and also assist with preparing the documents for a home loan. Furthermore, mortgage advisors can compare mortgage lenders in Germany to find a suitable home loan for expats in Germany.

If you want to review your individual mortgage options, you can contact Finance for Expats. We have also set up a Real Estate Search Engine to help you find properties within Germany and abroad. There you can search for apartments, houses and land to buy, sorted by price and other criteria.

Frequently Asked Questions About Mortgage Broker Germany

Do I need a mortgage broker in Germany?

For simple profiles, such as stable employment in Germany, strong equity, clean credit history, simple real estate and an existing banking relationship, it can be enough to go directly to German banks. Expats with foreign income, foreign earnings that have not been paid out in Germany yet, thin credit files and more complex situations are often better off being represented by a mortgage broker for expats.

Is a mortgage broker Germany free?

Many mortgage advisors get paid by the lender only. So there are no direct costs for the clients in many cases. Nevertheless, it is a good question to ask how someone is getting paid when doing business with you.

What is the difference between a mortgage broker Germany and a mortgage advisor Germany?

A mortgage broker is someone who searches through different mortgage providers to find a suitable mortgage for a given client. A mortgage advisor explains the advantages and disadvantages of the different types of mortgages in terms of risk, structure and affordability. Many companies have both mortgage brokers and mortgage advisors in their staff, which means that one company can help search for a home loan as well as helping to obtain approval for the home loan found.

Can foreigners get a mortgage in Germany?

Yes. As a foreigner you can get a mortgage in Germany. The criteria for mortgage approval in Germany are income, residence status, equity, "SCHUFA" and the property. There are, however, some mortgage lenders who are more experienced in dealing with international profiles than others.

How much deposit is required for a home loan Germany?

As a rule, a deposit of 20 percent to 30 percent of the purchase price for a home loan Germany may be required. In addition to this, purchase costs of around 7 percent to 12 percent of the purchase price for a home in Germany often have to be paid. For a property costing 300,000 euros, this could mean around 60,000 to 90,000 euros in equity plus roughly 21,000 to 36,000 euros in additional purchase costs, depending on the federal state and transaction structure.

Does SCHUFA affect mortgage approval in Germany?

A negative "SCHUFA" record or even an incomplete credit record can make mortgage approval more difficult. Likewise, a large number of unstructured applications can pose a risk.

Should I use a mortgage calculator before contacting a mortgage broker Germany?

A Germany home loan calculator is always useful for getting a first impression of your possibilities for getting a mortgage approved in Germany. However, we would recommend getting in touch with a mortgage broker as well to get a detailed offer for your mortgage in Germany.

How long does mortgage approval take in Germany?

Mortgage approval in Germany typically takes one to three weeks. At first, the lender may give you an initial offer within a few days after you have handed over the complete documents. However, full mortgage approval, which also includes the valuation of the property, typically takes longer.

Final Thoughts: Finding the Right Mortgage Support in Germany for Your Home Loan Approval

The right mortgage support for your mortgage in Germany largely depends on your individual profile. Simple German employment income and foreign income of expats are processed in completely different ways.

Whether you are a simple German employment case or an expat with foreign income, the right mortgage support in Germany is about approval, structure, risk and mortgage rates.

Before you start looking for a home, find out what your options for financing a home purchase are. For a first discussion and rough estimation, you can use our free Property Investment Calculator and/or a interest and repayment calculator for Germany. For a detailed mortgage plan and a variety of financing options, it is sensible to contact a mortgage broker or an independent mortgage advisor.

Finance for Expats in Germany can support you with the entire process. Contact us if you want to review your mortgage readiness before making an offer.