When people think about buying property in Germany, they usually focus on prices, mortgage rates and down payments. SCHUFA often comes up late in the process, sometimes only after a financing request has already failed. As a financial expert working with buyers and expats in the German real estate market, I can say this clearly: in 2026, SCHUFA is no longer a side detail. It is one of the most decisive factors for mortgage approval.

With changes to the SCHUFA score model and increasing risk awareness among banks, 2026 marks a turning point. Buyers with solid income still get rejected, while others with average income but clean credit profiles secure strong financing terms. This article explains SCHUFA 2026 in a practical way, what the new score model means, and how it directly affects your ability to finance property in Germany.

Table of Contents

- What SCHUFA is and how it works

- Why SCHUFA is critical for mortgage approval

- The new SCHUFA score model explained

- SCHUFA 2026 in mortgage practice

- Common SCHUFA mistakes buyers make

- SCHUFA for expats in Germany

- How to improve your SCHUFA score before buying

- SCHUFA, mortgage rates and buying power

- Should you delay buying because of SCHUFA

- Next step

What SCHUFA is and how it works

SCHUFA is Germany’s main credit bureau. Its role is to assess the probability that a person will meet their financial obligations. It does not judge character, income level or nationality. It calculates risk based on statistical models.

The data used includes existing contracts, payment history, account longevity and negative events such as defaults. Importantly, SCHUFA does not know your salary or your assets. This often surprises buyers who assume high income automatically means a good score.

From a bank perspective, SCHUFA is a first filter. Before a detailed mortgage calculation even starts, the credit profile is checked. If that profile signals elevated risk, the conversation often ends immediately.

Why SCHUFA is critical for mortgage approval

In 2026, banks are more cautious than in the past. Regulatory pressure and higher capital costs mean that risk assessment is stricter. SCHUFA plays a central role in this process.

In practice, SCHUFA affects three things. First, whether a mortgage application is approved at all. Second, which banks are willing to make an offer. Third, the interest rate and conditions attached to that offer.

I have seen cases where two buyers purchase similar properties at the same time. Same price, same down payment, same income range. The buyer with the cleaner SCHUFA profile received better conditions and faster approval. The difference was not the property. It was credit behavior over several years.

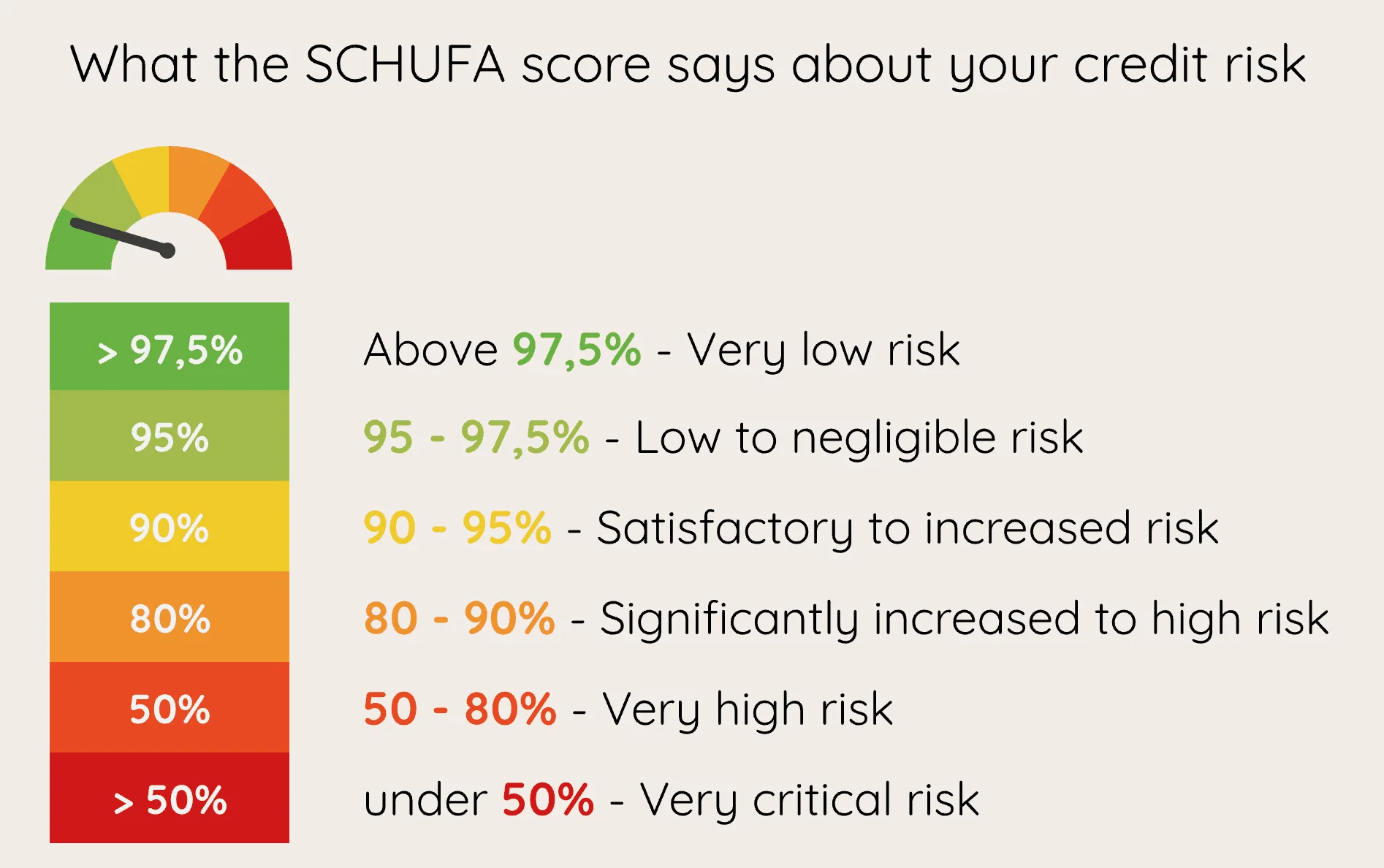

The new SCHUFA score model explained

Why SCHUFA updated its scoring approach

SCHUFA faced growing pressure to improve transparency and consumer understanding. Many people did not know why their score changed or what actions actually mattered. The updated model aims to simplify communication and make risk categories clearer.

What is different in the new SCHUFA score model

The new model focuses on clearer score ranges and simplified feedback. Instead of opaque percentage values alone, risk categories become more understandable. This does not mean the system is less strict. It means the signals are easier to interpret.

For buyers, this is positive. It becomes clearer which behaviors help and which hurt. However, the underlying logic remains unchanged. Consistency, reliability and long term stability are rewarded.

Why 2026 is the key year

The transition to the new model happens gradually. By 2026, most banks integrate the updated SCHUFA logic into their internal systems. That makes 2026 the year when buyers feel the impact most clearly, especially in mortgage decisions.

SCHUFA 2026 in mortgage practice

What is a good SCHUFA score for a mortgage

There is no single magic number. Different banks apply different thresholds. In general, a strong SCHUFA profile signals low risk and increases approval chances. A weak profile does not always mean rejection, but it limits options and raises costs.

How SCHUFA affects mortgage rates

Even when a mortgage is approved, SCHUFA influences pricing. Banks apply risk premiums. That means a weaker score can translate into higher interest rates, sometimes over decades. Over the life of a loan, this difference can amount to tens of thousands of euros.

This is why SCHUFA often matters more than headline mortgage rates you see online.

Common SCHUFA mistakes buyers make

The most common mistake is ignoring SCHUFA until it is too late. Buyers focus on property search and financing talks, only to discover that their credit profile limits everything.

Another frequent issue is having too many accounts or credit cards. While none of them may be problematic individually, the overall structure signals higher complexity and risk.

Closing old accounts too quickly is also a mistake. Long credit history is valuable. Removing it can reduce stability signals.

SCHUFA for expats in Germany

Expats often start with a weaker SCHUFA profile simply because they are new to the system. Short credit history, few long term contracts and recent address changes all reduce score stability.

This does not mean expats cannot get mortgages. It means preparation is essential. Establishing a clean payment record, keeping accounts stable and avoiding unnecessary credit products helps significantly.

When expats plan early, SCHUFA becomes manageable rather than a barrier.

How to improve your SCHUFA score before buying

Six to twelve months before applying

The best time to improve SCHUFA is well before you apply for a mortgage. This allows changes to be reflected properly.

Pay all obligations on time. Reduce unnecessary accounts. Avoid frequent address changes. Keep existing accounts stable.

Checking and correcting data

Errors happen. Incorrect entries can exist. Checking your data early allows time to request corrections. This alone can sometimes improve a score meaningfully.

SCHUFA, mortgage rates and buying power

SCHUFA does not exist in isolation. It interacts with mortgage rates and affordability. A weaker score can reduce buying power even when income is strong.

To understand how financing conditions affect your long term numbers, the Property Investment Calculator can help translate rates and loan structures into realistic scenarios: https://financeforexpats.de/property-investment-calculator.

Likewise, exploring realistic properties before financing discussions helps avoid frustration. The Real Estate Search Engine allows you to compare options based on actual market conditions: https://financeforexpats.de/real-estate-search-engine.

Should you delay buying because of SCHUFA

Delaying a purchase can make sense if SCHUFA issues are temporary and fixable. A few months of preparation can significantly improve conditions.

Delaying does not help if issues are structural, such as repeated defaults or unresolved disputes. In those cases, a different strategy may be required.

The key is clarity. Guessing rarely helps.

Next step

SCHUFA 2026 is not about fear. It is about preparation. Buyers who understand their credit profile early gain control and flexibility. Those who ignore it often lose options.

If you want to assess how your SCHUFA profile affects your mortgage options and property plans, a structured review can save time and money. You can contact FFE for a personal consultation here: https://financeforexpats.de/contact.