Mortgage in Germany for Foreigners and Expats Explained

Thinking about buying property in Germany but not sure if your residency status gets in the way? You're not alone. This is one of the most common questions expats ask, and the short answer is more encouraging than many people expect.

A mortgage in Germany is absolutely achievable for foreigners, even without permanent residency. What matters far more to most lenders is whether you can afford the loan, how stable your income is, and how much deposit you're bringing to the table. Residency status plays a role, but it's rarely the single deciding factor. This article gives you a clear, realistic picture of what to expect before you start the process if you are looking for a mortgage in Germany for foreigners or expats.

Why Expats Want to Buy Property in Germany Before Permanent Residency

Renting in cities like Munich, Frankfurt, or Berlin has become increasingly expensive. Many expats who plan to stay for several years reach a point where paying rent month after month starts to feel like dead money, especially when a home loan in Germany could be putting that same cash toward an asset they actually own.

Buying property can build long term financial stability, provide a sense of roots, and protect against rental market volatility. Waiting years for permanent residency before even exploring the Germany property market simply doesn't make sense for a lot of people, particularly those on strong incomes with solid savings already in place. For many buyers, a home loan in Germany for foreigners is the practical route into ownership.

Can You Get a Mortgage in Germany Without Permanent Residency

Yes, you can. Many banks and lenders in Germany do finance foreign buyers who don't yet hold permanent residency. That said, not every lender approaches this the same way. Some are more cautious with non EU applicants, while others focus almost entirely on financial strength regardless of passport or residency type.

If your mortgage in Germany application shows stable employment, a clean financial profile, and a reasonable deposit, you'll find doors that open. Strong applicants consistently receive better options and more competitive rates. Weaker profiles may face additional hurdles, but that applies to German applicants too. The key is understanding what banks actually look at before they decide. There is no single best mortgage Germany for foreigners, because the right offer depends on your income, deposit, property type, and the lender's own criteria.

What German Banks Check Before Approving a Mortgage

German lenders are thorough. They assess risk carefully, and understanding their criteria helps you prepare properly before submitting any application for a German mortgage.

Monthly net income and employment stability are assessed first. Banks want to see that your income reliably covers living costs and the new mortgage repayment with room to spare. They'll also look at any existing debts, fixed expenses like car finance or subscriptions, the deposit you've saved, the quality and location of the property, and your overall financial behaviour over time.

Income and Employment Stability

If you're on a permanent contract, that typically helps your home loan in Germany application. Fixed term contracts are not automatically disqualifying, especially if you're in a high demand profession or earning a strong salary. Probation periods can make things harder in the short term, so if you're early in a new job, it may be worth waiting until that period ends before applying.

Credit Score in Germany and SCHUFA

Most German lenders check SCHUFA, which is the local credit reference system. If you've recently moved to Germany, you may have little or no SCHUFA history, which sounds alarming but doesn't always lead to rejection. Your credit score in Germany is one factor among several. A larger deposit or higher income can offset a thin credit file in many cases. Building some SCHUFA history early through a bank account or mobile contract is a sensible move regardless. A stronger credit score Germany for mortgage approval can make a real difference when banks compare similar applications.

Deposit Size and Affordability

A larger deposit reduces the lender's exposure and often unlocks better terms. Using a mortgage calculator Germany before you speak to any bank helps you understand what monthly payments look like based on different loan sizes and rates. Buyers who arrive at conversations with a realistic grasp of their numbers tend to get further faster.

How Much Deposit Do You Need to Buy Property in Germany

Most buyers in Germany aim for at least 10 to 20 percent of the purchase price as a deposit. A larger contribution generally improves your position when applying for a mortgage in Germany. However, deposit alone doesn't tell the full story. You also need to budget for purchase costs on top of your deposit, which typically run between 9 and 12 percent of the purchase price depending on the federal state.

Many expats ask how much deposit for mortgage Germany is really needed. In practice, the answer is not just the bank minimum. You also need enough cash to cover buying costs separately.

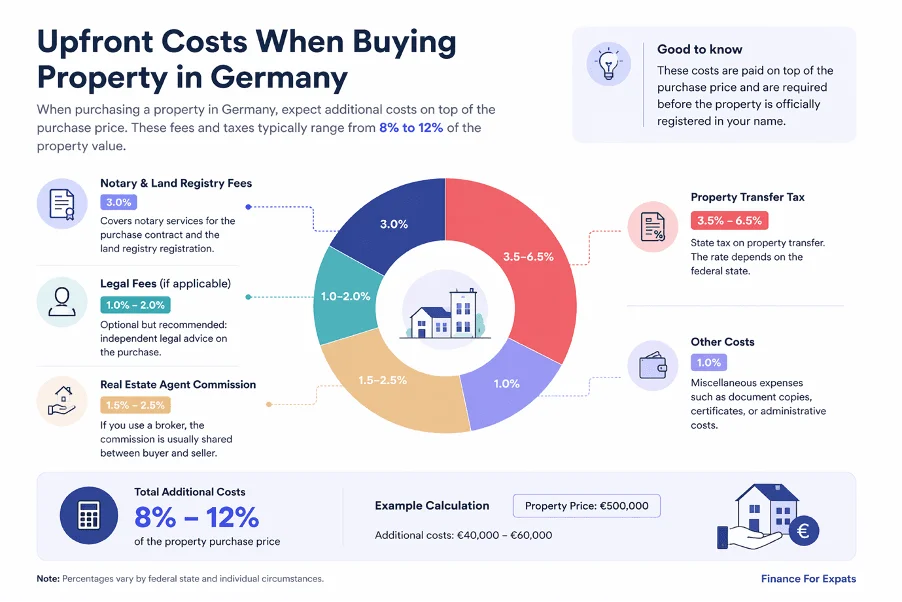

Upfront Costs When Buying Property in Germany

The main additional costs include property tax in Germany, known as Grunderwerbsteuer, notary fees, land registry fees, and if you use an estate agent, their commission. These costs are paid from your own savings and cannot usually be rolled into the mortgage. Knowing this upfront avoids nasty surprises and helps you plan your total cash requirement accurately.

Mortgage Rates in Germany for Foreigners

Mortgage rates in Germany are influenced by the European Central Bank's policy rate, your lender's own risk assessment, the size of your loan relative to the property value, and your overall financial profile. Being a foreigner doesn't automatically push your rate higher. What matters more is how your application looks on paper.

Fixed rate German mortgage products are by far the most common choice in Germany. Borrowers tend to prefer the certainty of knowing exactly what they'll pay for the next 10 or 15 years.

Current Mortgage Interest Rates in Germany

Current mortgage interest rates in Germany shift with broader market conditions and ECB decisions. What was a good rate two years ago may look quite different today, which is why comparing offers regularly makes sense. Even a small difference in rate can translate to thousands of euros over the life of a loan. Getting updated figures from multiple sources before committing is always worth the time.

Anyone comparing current mortgage rates Germany today should keep in mind that lenders price risk differently depending on deposit size, income stability, and property type.

Mortgage Calculator Germany: How Much Can You Afford

Before calling a single bank, spend some time with a mortgage calculator Germany. These tools let you input your income, deposit, and expected loan amount to get a rough picture of what monthly repayments might look like. A Germany mortgage calculator helps you move from guesswork to realistic numbers quickly.

If you're earning €5,000 net per month and have €60,000 saved as a deposit, a German mortgage calculator helps you figure out whether a €350,000 property is within reach or whether you should adjust your search range. Going into conversations with banks already knowing your numbers puts you in a much stronger position. Many buyers start with a mortgage calculator Germany expat search, and a home loan calculator Germany or house loan calculator Germany can be a useful first step before speaking with a bank or broker. For a more detailed estimate, try our mortgage interest and repayment tool.

Mortgage Broker Germany vs Direct Bank Application

You have two main routes: apply directly to a bank, or work with a mortgage broker Germany. Brokers compare products across multiple lenders and can often find deals that aren't advertised publicly. For expats, an English speaking broker can make the entire process far less stressful, particularly when navigating documentation in a second language.

Direct bank applications work well for straightforward profiles. If your finances are clean and uncomplicated, going direct can be perfectly fine. For more complex situations, non standard employment, limited German banking history, or simply wanting to compare multiple offers, a German mortgage broker typically adds real value. For many international buyers, an English speaking mortgage broker Germany option is especially useful.

Germany Property Market: Is Buying Worth It for Expats

The Germany property market has had its ups and downs in recent years, but long term ownership still tends to benefit those who buy with realistic expectations and a clear plan. Comparing buying versus renting over a ten or fifteen year horizon usually paints a more favourable picture for buyers than short term housing market Germany headlines suggest.

Location and budget matter far more than market noise. If you're serious about exploring what's available, using a Real Estate Search Engine to browse real properties and understand local pricing gives you a concrete starting point. Many buyers who are learning how to buy property with mortgage in Germany begin here, because financing decisions make more sense once you understand real asking prices.

Property Tax Germany and Other Buying Costs

The mortgage Germany repayment itself is only part of what you'll pay. Property tax in Germany continues as an annual cost after purchase, alongside building insurance, maintenance reserves, and potentially service charges if you're buying in a shared building. Using a Property Investment Calculator helps you model the true cost of ownership before you commit.

Understanding property tax Germany for homeowners is especially important if you're budgeting only for the mortgage payment and not the full long term cost of ownership.

Common Reasons Mortgage Applications Get Rejected

Even strong candidates can face rejection if something has been overlooked. The most common reasons include a deposit that's too small, an unstable income, high existing personal debts, poor affordability, missing documentation, and properties considered risky due to location or condition. Understanding these traps before applying for a mortgage Germany can save time and prevent marks on your credit score Germany from declined applications.

How to Improve Your Mortgage Chances in Germany

Building the strongest possible application before approaching any bank is the smartest move. Increase your deposit if you can. Reduce outstanding personal debts. Gather clean and complete financial documentation. Run your numbers through a mortgage calculator Germany to check affordability honestly. Compare multiple lenders rather than accepting the first offer you receive. Working with a mortgage broker Germany can simplify this process considerably. If you want tailored guidance for your specific situation, reaching out through our contact page for personal support can help you move forward with confidence.

FAQs About Mortgage in Germany for Foreigners

Can foreigners buy property in Germany

Yes. Foreigners can generally purchase property in Germany without citizenship restrictions. Both EU and non EU nationals are permitted to buy.

Do I need permanent residency to get a mortgage in Germany

No. Many lenders finance applicants without permanent residency when the financial profile is strong enough.

How much deposit do I need for a mortgage in Germany

Most buyers aim for at least 10 to 20 percent of the purchase price, plus enough cash to cover purchase costs separately.

Are mortgage rates in Germany fixed or variable

Fixed mortgage rates Germany are the more popular choice, offering repayment certainty over the loan term.

How do I check my credit score in Germany

You can request your SCHUFA data through official approved providers. It's worth doing this before you apply for any loan.

Should I use a mortgage broker in Germany

If you want to compare multiple lenders or prefer English speaking support, a mortgage broker Germany is usually a good investment of your time.

What is the best mortgage in Germany for foreigners

There is no single best mortgage in Germany for foreigners. The best option depends on your income, deposit, residency status, property type, and the lender’s requirements.

Final Thoughts on Getting a Mortgage in Germany

Permanent residency helps, but it's far from the only thing lenders care about. A well prepared application with strong income, a solid deposit, and clean finances will open more doors than most expats expect. The mortgage Germany process rewards preparation. Start early, compare your options, understand your numbers, and don't assume rejection before you've tested the market. The right home loan Germany might be closer than you think.