Germany mortgage rates in 2026 are a hot topic for buyers, expats, and real estate investors. After the ultra low era ended and financing costs reset, many people are asking the same practical questions: will mortgage rates go down in Germany in 2026, what is a realistic mortgage rate forecast for Germany 2026, and when is the best time to fix a mortgage rate in Germany.

I work with clients who buy and finance property in Germany every day. The most common mistake I see is trying to wait for the perfect rate. In the German market, the winning strategy is rarely timing a single moment. It is building a financing structure that still works if rates move slightly up, slightly down, or sideways.

This article gives you a realistic Germany mortgage rates 2026 outlook with scenarios, practical rate fixing strategy, and a visual forecast chart you can use to make decisions. It is written for people who want clarity and a plan, not a headline.

Table of Contents

- Germany mortgage rates 2026 overview

- What drives mortgage rates in Germany

- Mortgage rate forecast Germany 2026

- Fixed rate versus variable mortgage rates Germany 2026

- Best time to fix your mortgage rate in Germany 2026

- Mortgage rates for expats in Germany 2026

- Monthly payment impact and buying power

- Buy property in Germany 2026 or wait

- Germany mortgage rates 2026 for investors

- Common mortgage rate mistakes in Germany

- FAQs Germany mortgage rates 2026

- Next step

Germany mortgage rates 2026 overview

Germany mortgage rates in 2026 are no longer anchored near zero, but they are also not in a panic zone. The market has adapted. Banks price mortgages with a more normal cost of capital, and borrowers plan with more realistic budgets. In plain terms, the conversation in 2026 is less about shock and more about structure.

Most mortgages in Germany are built around fixed interest periods. That is why people often search for fixed rate mortgage Germany 2026, ten year mortgage rate Germany, or fifteen year fixed mortgage Germany. German borrowers typically value stability. This matters because the best mortgage strategy in 2026 depends on the length of your fixation period, your down payment, and how much buffer you keep in your monthly budget.

If you want to explore real listings and build a realistic view of what your budget can buy in different regions, the Real Estate Search Engine is a practical starting point.

What drives mortgage rates in Germany

ECB policy and market expectations

The European Central Bank influences the interest rate environment, but German mortgage rates do not move in a simple one to one relationship. Banks price mortgages based on expectations about future policy, inflation, and long term funding costs. That is why mortgage rates can move even when the ECB does nothing, and why the mortgage rate forecast Germany 2026 is more about market expectations than about a single meeting.

Inflation expectations and long term confidence

Inflation is not just a statistic. It is the story lenders tell themselves about the next decade. If inflation expectations are stable, long term rates tend to stabilize too. If inflation expectations rise again, long term rates can climb quickly, even if short term data looks calm.

Bond yields and the Pfandbrief channel

German mortgage lending is closely connected to long term bond yields and the Pfandbrief market. Pfandbriefe are covered bonds used to fund mortgages. When long term yields move, mortgage pricing moves. This is one reason the German mortgage market prefers fixed interest periods and conservative underwriting.

Bank risk premiums and borrower profile

In 2026, banks remain careful with risk. Loan to value, stable income, property type, and borrower documentation all affect the final offer. Two buyers can see different mortgage rates even on the same day. This is why chasing a headline rate is less useful than building a strong borrower profile.

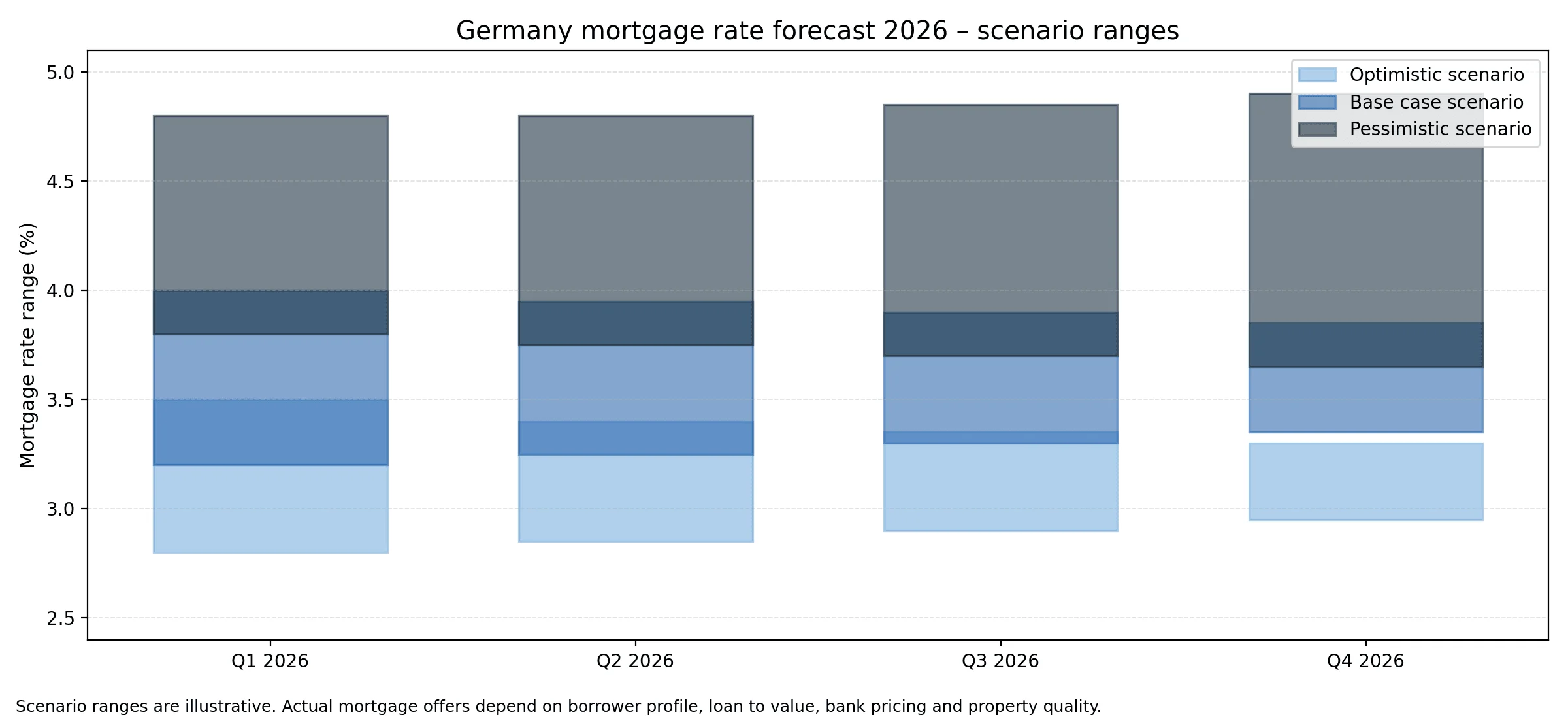

Mortgage rate forecast Germany 2026

Before we talk strategy, we need to separate two things. A forecast is not a promise. The practical way to think about Germany mortgage rates 2026 is through scenarios. Scenarios help you plan. Predictions invite disappointment.

The graphic below shows three scenario ranges for Germany mortgage rates 2026. It is intentionally range based. Real mortgage rates depend on your down payment, the bank, the property, and your financial profile. Use it as a decision tool, not as a guarantee.

How to read the mortgage rate forecast Germany 2026 chart

The base case range represents a stable to slightly lower environment. This is the scenario where inflation expectations remain contained and the bond market stays calm. In this environment, mortgage rates in Germany 2026 can fluctuate, but the overall level remains broadly manageable for prepared buyers.

The optimistic range shows a moderate decline path. This requires a supportive macro backdrop and continued confidence that inflation is under control. If this happens, strong borrowers with solid equity can benefit first, because banks tend to reward low risk profiles when rates drift down.

The pessimistic range represents renewed upward pressure. It is not about panic. It is about the reality that inflation can re accelerate, risk premiums can rise, and markets can reprice quickly. The main value of the pessimistic range is to help you answer one question: if rates move up, does your plan still work.

What the chart implies for the best time to fix your rate

If you can only afford your purchase in the optimistic range, you are betting on rate timing. That is fragile. If your budget works in the base case range and still survives the pessimistic range with a smaller buffer, you have a resilient plan. In German real estate financing, resilience often beats perfect timing.

Fixed rate versus variable mortgage rates Germany 2026

Fixed rate mortgage Germany 2026

Fixed rate mortgages dominate in Germany because they reduce uncertainty. Ten year, fifteen year, and twenty year fixed periods are common. In 2026, many buyers prefer longer fixation because it makes monthly costs predictable and protects against a rate rebound.

In client meetings, I often use a simple story. Two buyers purchase similar apartments. One locks a longer fixation and sleeps well. The other chooses a shorter fixation to chase a slightly lower rate and spends years worrying about refinancing. The second buyer often pays more in stress than they ever saved in interest.

Variable mortgage Germany 2026

Variable rates can be useful in specific cases, such as short holding periods, high planned repayments, or bridge financing. But variable mortgages require buffers and discipline. If you choose variable rates, you must be comfortable with uncertainty and you must have a plan for adverse moves.

Best time to fix your mortgage rate in Germany 2026

The best time to fix your mortgage rate in Germany 2026 is when three conditions are met. Your monthly payment fits your budget with a buffer. Your financing structure fits your life plan. And your plan still works even if rates do not drop.

Rate timing versus rate readiness

People love the idea of timing. In practice, readiness matters more. Readiness means your documents are complete, your down payment is clean, your property choice is realistic, and you can move quickly when a good opportunity appears. The buyer who is ready often wins the better property and negotiates better terms, even if rates are not perfect.

Forward loans and securing a rate

If you refinance in 2026, a forward loan can sometimes help you secure terms earlier. The trade off is cost. You pay for the right to lock a rate. Whether that makes sense depends on your remaining fixed period, your risk tolerance, and your cash flow buffer.

Mortgage rates for expats in Germany 2026

Expats can finance property in Germany, but bank criteria vary. Some lenders are comfortable with international income and strong documentation. Others prefer local employment and longer residency. It is common for banks to scrutinize expat applications more closely, especially when income is foreign or when the residency outlook is uncertain.

In practice, expats can often improve conditions by preparing a clear file. Stable income documentation, a strong down payment, and a realistic loan to value can matter more than nationality. The keyword here is credibility. Banks price risk, and credibility reduces risk.

Monthly payment impact and buying power

Mortgage rates do not matter in isolation. They matter because they change monthly payments and buying power. Even small rate moves can change affordability. This is why the scenario chart above is useful. It tells you what to test.

If you want to translate rates into monthly payment scenarios and long term outcomes, use the Property Investment Calculator. It helps you see how financing costs affect cash flow, yield, and long term stability.

Buy property in Germany 2026 or wait

Reasons buying in 2026 can make sense

In many markets, buyer competition is lower than in the boom years. That can improve negotiation and reduce emotional bidding. If you find a high quality property at a fair price and your financing is resilient in the base case scenario, buying can be rational even without perfect rates.

Reasons waiting can be sensible

Waiting can be smart if your finances are not ready, your down payment is thin, or your job situation is uncertain. Waiting is less smart if it is purely a bet that rates must drop. In Germany, property selection and financing structure often create more value than guessing the next rate move.

If you want to scan opportunities across regions and compare what fits your criteria, the Real Estate Search Engine can help you build a realistic shortlist.

Germany mortgage rates 2026 for investors

For investors, Germany mortgage rates 2026 matter because they affect cash flow and leverage. When rates are higher, the margin for error is smaller. That does not mean investing stops. It means the strategy becomes more conservative.

Investors should focus on strong locations, realistic rent assumptions, and conservative financing. The best investors I know treat financing as a stability tool, not as an aggressive lever. In 2026, that mindset is rewarded.

Common mortgage rate mistakes in Germany

Chasing the lowest rate and ignoring the structure

The lowest rate is not always the best deal. Flexibility, repayment options, and a realistic buffer can be more valuable than a slightly lower nominal rate.

Underestimating refinancing risk

Short fixation can look cheaper today, but it shifts risk to the future. If your plan depends on refinancing at a lower rate later, you are making a second bet you cannot control.

Ignoring the borrower profile factor

Many people search for the best mortgage rates Germany 2026 and assume there is one number. In practice, your number depends on your profile. Improve the profile, and the rate often improves.

FAQs Germany mortgage rates 2026

Will mortgage rates go down in Germany in 2026

They can move down, but the base case is stability with moderate fluctuations. Plan with scenarios rather than certainty.

What is a good mortgage rate in Germany 2026

A good rate is one that fits your long term plan and still works if rates move against you. The best rate is useless if it forces you into an unstable budget.

Should I choose fixed rate or variable rate mortgage in Germany 2026

Most buyers prefer fixed rate mortgages for stability. Variable rates can be appropriate for specific strategies with strong buffers.

How long should I fix my mortgage rate in Germany

Ten to fifteen years is common, and longer periods can be attractive if you value stability. The right answer depends on your income outlook and risk tolerance.

Do expats pay higher mortgage rates in Germany

Sometimes, but many expats can secure strong offers with good documentation, solid equity, and stable income.

Next step

If you want to apply the mortgage rate forecast Germany 2026 scenarios to your personal situation, it helps to review your numbers, your buffer, and your financing structure. A short consultation can prevent expensive mistakes and clarify whether you should fix now, wait, or adjust the purchase plan.

You can contact FFE here.