Table of Contents

- Introduction: Why Expats Buy Property in Germany

- How to Buy Property in Germany Step by Step

- Biggest Mistakes Expats Make When Buying Property in Germany

- Property Costs Germany: What You Must Calculate

- Understanding the Germany Real Estate Market

- Financing Property in Germany as an Expat

- What to Check Before Buying Property in Germany

- Is Buying Property in Germany Worth It?

- Frequently Asked Questions

- Final Thoughts: Buying Property in Germany Without Costly Mistakes

This is your complete, practical guide to buying property in Germany as an expat. It covers everything you need to know about purchasing a property in a clear step by step guide. We have written this guide to give you a realistic view of what buying property in Germany is like. The guide covers all the key elements of the property buying process, hidden charges, legal framework, financing, property documents Germany buyers should check, and more.

Buying property in Germany can be one of the best long term decisions for expats, but it can also become expensive if you misunderstand documents, costs or financing before signing the notary contract. This guide helps you understand the structure behind buying property Germany, so you can avoid costly mistakes before they happen.

Buying property in Germany is not only about finding a nice apartment or house. It is about understanding the structure, the costs, the documents, the mortgage and the risks before signing anything. We hope that this guide will give you enough information and confidence to find and purchase your dream home or investment property in Germany.

Why Expats Buy Property in Germany

The Germany real estate market offers a wide range of opportunities for foreign buyers and international investors. Germany has a very stable economy, strong demand for rental apartments, and a fair and well organized legal system. Compared with many other countries, real estate Germany is often seen as a conservative, long term investment rather than a fast speculation market.

Germany is also a nation of renters. In many major cities, rental demand remains high, especially in places where population growth, job opportunities and limited housing supply meet. This makes the German real estate market attractive for expats who want to live in their own home, buy an apartment in Germany, buy a house in Germany, or invest in property Germany for the long term.

But buying real estate in Germany as a foreigner is not always easy. There are many possible problems during the purchase process. First of all, it is necessary to find the right property for sale in Germany. A good Real Estate Search Engine is the perfect start for your property search, especially if you want to compare properties, locations and price levels more efficiently. But even after you have found the perfect property for sale in Germany, there is still a real chance that things can go wrong during the buying process if you are not prepared.

How to Buy Property in Germany Step by Step

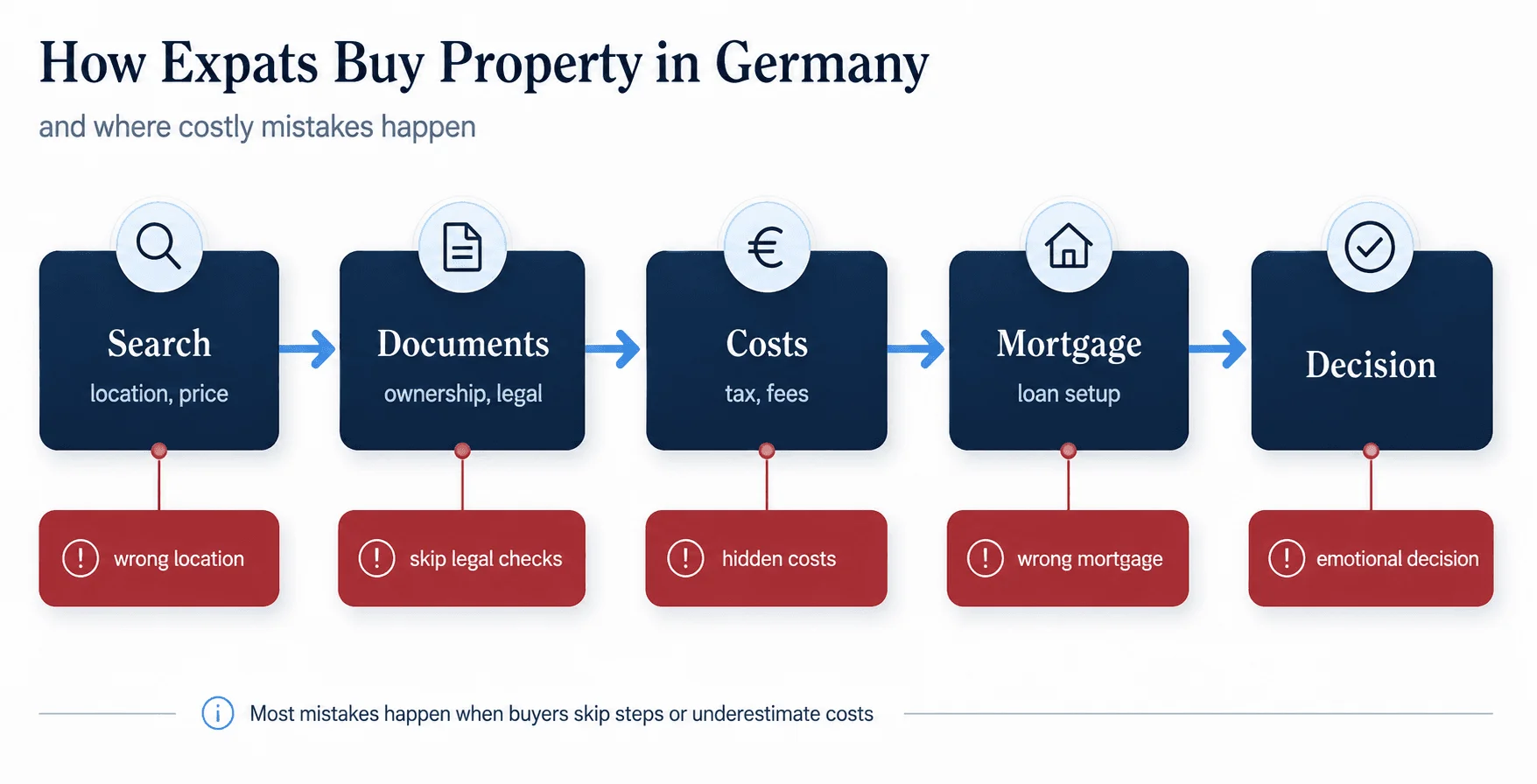

Here is a simple summary of the steps. With every step, mistakes can occur. For expats, the important point is not only knowing the order of the process, but understanding where risk, cost and financing problems can appear.

Step 1: Find a Property

First of all, you need to find the right property. This can be done by contacting local estate agents, searching on property portals, using a Real Estate Search Engine , or looking at properties at real estate auctions. After finding a suitable property, it is recommended to view it in person. After viewing a couple of properties, you can then start to shortlist your favorites in order to proceed with the next steps.

Step 2: Check the Documents

Next, check all documents. Especially important is the land register, called the "Grundbuch". It shows who the owner of a property is and whether there are any outstanding loans, rights of use, building restrictions or other legal entries. It can happen that previous debts or restrictions are registered on the property and need to be checked before signing.

It is also important to check the declaration of division, called "Teilungserklärung", for apartments in buildings divided into multiple units. The "Aufteilungsplan" is a floor plan that outlines the layout of individual units in such a property. These documents are very important in order to clarify what a buyer actually buys, which areas are privately owned, which parts are shared, and what restrictions may apply.

Step 3: Secure Financing

Before starting serious negotiations, secure a pre approval for a loan from a bank or mortgage broker. As a foreigner, it can be difficult to gain a clear impression of your credit worthiness, because the bank will check your income, equity, residence status, SCHUFA and overall financial profile.

The pre approval should state the approximate amount for which you may be approved and for how long the approval is valid. This helps you understand your real budget before making an offer. It also protects you from looking at properties that do not fit your mortgage Germany approval reality.

Step 4: Sign the Notary Contract

The notary, called "Notar", usually draws up the purchase contract. The contract is then signed by both parties in the presence of the notary. Only a notarized contract is legally valid for buying property in Germany. Private purchase contracts for real estate are not valid.

Step 5: Transfer Ownership

After payment of the property purchase price and the settling of all taxes and fees, the notary will register the new owner of the property in the "Grundbuch". Only after the land register entry has been completed does the buyer become the official owner.

Biggest Mistakes Expats Make When Buying Property in Germany

Before you spend any money on the purchase of German properties of any kind, such as houses, apartments or investment properties, you should understand where most mistakes happen. The biggest mistakes foreign property buyers in Germany make usually fall into three groups:

- Legal documents of German real estate for foreign buyers

- Property purchase costs of German real estate

- Property financing of real estate Germany for foreigners

The following graphic show the full buying process and highlight where mistakes can happen: property search, document checks, cost calculation, mortgage approval, notary contract, ownership transfer and long term ownership.

Skipping Property Documents Germany Checks

The "Grundbuch", also called land register, is one of the most important documents to check before you buy property in Germany. It states who the owner of a property is, whether there is any outstanding debt on the property, for example a mortgage, and whether there are any rights of use, such as a right of way for another person, or other restrictions on the use of the property.

Before you sign the contract for the purchase of a property, it is very important to check the "Grundbuch" in detail. Many buyers fail to do this because the terms used are formal German. Ask your notary, lawyer or advisor to explain the terms to you before you sign the purchase contract.

For apartment purchases in Germany, it is also necessary to check the so called "Teilungserklärung" and "Aufteilungsplan". The "Teilungserklärung" is a notarized document which defines the individual property units within an apartment building and the shared elements. The declaration also includes the rules of the building community, known as "Wohnungseigentümergemeinschaft". The "Aufteilungsplan" is the floor plan of the individual property units.

As the owner of an apartment in Germany, you are bound by the conditions of the property documents as soon as you have signed the notarial purchase contract. It is therefore important to check the property documents very carefully, ideally with the help of a bilingual lawyer or experienced property advisor.

Underestimating Property Costs Germany

The purchase price of a property does not equal the real cost of buying property in Germany. Additional costs, referred to as "Kaufnebenkosten", must be paid on top of the agreed purchase price. The most expensive of these is usually the "Grunderwerbsteuer", the property transfer tax.

Typical property costs Germany buyers must calculate include:

- "Grunderwerbsteuer" Germany: usually 3.5 percent to 6.5 percent of the purchase price, depending on the federal state

- "Notarkosten" Germany: approximately 1 percent to 1.5 percent of the purchase price

- Land register registration fee: around 0.5 percent

- "Maklerprovision": often around 3 percent to 7 percent, depending on the agreement and property type

The total acquisition costs can amount to around 10 percent to 15 percent of the purchase price and need to be included in your affordability calculation. For example, on a 400,000 euro apartment, the transfer costs and agent commission can easily add tens of thousands of euros to the real purchase cost.

This is why it is important to use a Property Investment Calculator when discussing total costs, mortgage affordability and long term returns. What looks affordable based on the purchase price alone may become far less attractive once all acquisition costs and ongoing costs are included.

Misunderstanding Ongoing Costs: "Hausgeld" Germany

Many owners of apartments in Germany are unaware of the amount of the so called "Hausgeld". "Hausgeld" is the building management fee charged for shared expenses of the building. Other costs such as property insurance, "Grundsteuer" and "Instandhaltungsrücklage" are also often ignored by buyers.

The total building management fees are usually published in the property description. However, it is not uncommon for the amount to increase after the purchase. High maintenance costs can quickly eat into the returns of a property that initially seemed to be a good purchase.

It is not enough to request only the last annual statement. In addition, it is advisable to request the account statements for the last three years in order to see the development of the "Hausgeld". Also ask for the current balance of the "Instandhaltungsrücklage", the sinking fund for maintenance. If the reserves are not sufficient to cover major repairs such as roofs, elevators or facade works, you can be charged with a Sonderumlage. This special levy can reach thousands of euros for one property.

Choosing the Wrong Mortgage Germany Structure

The German home loan market offers different mortgage structures. The most common type of loan is the fixed rate annuity loan, known in German as "Annuitätendarlehen". With this home loan Germany structure, the fixed interest rate is defined at the beginning of the term for a fixed period, typically 10 to 20 years.

Expats are often mistaken when selecting the fixed term and repayment structure. Many homebuyers initially calculate their returns based only on the purchase price. In reality, Kaufnebenkosten are often paid from the buyer’s equity. Many lenders require a down payment of at least 20 percent of the purchase price plus the full amount of Kaufnebenkosten.

There are also variable interest rate home loans available on the German market, but these include the risks associated with changing mortgage rates buyers need to understand. Choosing the wrong mortgage structure can create long term affordability problems, especially if interest rates change or if the buyer has not calculated enough financial buffer.

Buying in the Wrong Location: Property in Germany

The most important factor when determining capital growth and the return of an investment in housing in Germany is location. As with other property markets around the world, property prices can vary significantly from city to city and also from district to district.

Only some of Germany’s major cities have sufficient and stable demand for apartments in order to support long term value stability and rental demand. Cities such as Berlin, Munich, Hamburg, Frankfurt and Cologne are often attractive because of their economic strength and tenant demand. However, properties in these cities are also expensive and rental yields are often lower.

Smaller cities and regional markets can offer more attractive entry prices, but they may also carry higher risks if population trends, rental demand or local economic strength are weaker. The net return after depreciation, management costs, financing and maintenance is not automatically higher just because the purchase price is lower.

Property Costs Germany: What You Must Calculate

There are two categories of costs when buying a property in Germany: costs that are paid once and costs that are paid regularly every year. Many buyers look at the cost of the property, add the agent’s commission, and believe that they have included all costs. This is not the case. When you add the one time costs and the annual or monthly costs, you will see the real costs involved.

The acquisition costs for a property in Germany, called "Kaufnebenkosten", usually amount to around 10 percent to 15 percent of the purchase price. They often have to be covered by the equity used for the down payment.

Additional hidden risks for the property owner in Germany are the potential for a special levy, called "Sonderumlage", if the "Instandhaltungsrücklage" is underfunded. There is also the risk of expensive renovations to older buildings, including energy efficiency upgrades such as insulation of walls, roofs or heating systems.

Before making a decision, input all of the purchase price and ongoing costs into a Property Investment Calculator. This helps you work out the true return on your investment. You may realize that what initially seemed like a strong return actually becomes only a marginal return after all costs are included.

Understanding the Germany Real Estate Market

There is high demand and not enough supply for homes in many large German cities. For decades, not enough new housing has been built in several urban areas. This has contributed to high property prices for german buyers in popular locations.

However, the housing market in Germany is not the same everywhere. In some regions, especially outside the major economic centers, property prices can be lower. But lower prices alone do not automatically mean better investment opportunities. Demand needs to be checked carefully.

Since 2022, interest rates have increased significantly compared with the previous low interest period. This has reduced affordability and created a cooling effect in some parts of the property market. For well prepared buyers with solid financing, this can also create opportunities to buy a house or apartment at a fairer price than during overheated market phases.

Financing Property in Germany as an Expat

Home loans for foreigners are possible in Germany, but the approval process depends heavily on income, equity, residence status and risk profile. The main factor German banks take into consideration when reviewing a home loan application is income. This can be a permanent employment contract or tax returns for self employed individuals.

Banks will also consider the buyer’s SCHUFA credit score, Germany’s credit reference system. In terms of how much of a home loan a foreigner can obtain, a significant equity participation is usually required. In practice, expats often need to fund a down payment of around 30 percent to 35 percent of the purchase price including "Kaufnebenkosten" before a home loan can be granted.

Some banks do not grant home loans to non EU nationals or non residents at all. For those who are eligible for a home loan, the process can benefit from using a bilingual mortgage broker who is familiar with the situation of expats and who works with a variety of relevant lenders.

What to Check Before Buying Property in Germany

This is a minimal due diligence checklist for buying real estate in Germany. A more extensive list would include many more items, but the following checks are essential.

- Documentation: Verify ownership through the "Grundbuch" extract. For apartments, verify the property division through the "Teilungserklärung" and "Aufteilungsplan". Check the "Hausgeld" and building management documents.

- Other costs: Write down all costs linked to the purchase of a property in Germany, including "Kaufnebenkosten", notary fees, property transfer tax, land register fees and agent commission.

- Ongoing costs: Include the monthly "Hausgeld", property tax, maintenance reserves and possible future special levies.

- Condition: The buyer should make sure through an independent building expert that the building is in good condition. Serious defects can be financially damaging after purchase.

- Financing: Check the amount of pre approval that a bank or mortgage broker can provide. This tells you how much you can afford in total, including your equity and the maximum loan amount.

This checklist is not only about avoiding legal mistakes. It also helps you understand whether the property is financially sustainable. If one of these areas is unclear, it is better to slow down before signing than to discover the problem after the notary contract.

Is Buying Property in Germany Worth It?

Buying a house or apartment in Germany for the long term can be a sound investment for expats, but it is not a get rich quick strategy. Rental yields are generally lower in many German cities, often around 2 percent to 4 percent gross, and cash flow can become negative after service charges, taxes, financing and maintenance.

At the same time, Germany offers a secure legal environment, strong tenant demand in many regions and a relatively stable long term real estate market. Long term property investment Germany buyers pursue is usually based on stability, capital preservation and gradual value growth rather than fast returns.

Compared with renting, buying property in Germany can offer long term cost stability and the chance to build wealth through ownership. Renting gives more flexibility in the short term, but it does not provide the same opportunity to benefit from long term property value development.

Buying property in Germany is conservative, structured and often slow. But for expats with a long term perspective, strong financing and careful due diligence, it can work very well.

Frequently Asked Questions

Can foreigners buy property in Germany?

Yes. Foreigners can buy residential and commercial real estate in Germany. There is no general restriction on foreigners buying property in Germany. Whether you are from within the EU or outside the EU, you can buy property in Germany under the same ownership rules as German buyers.

How much money do you need to buy property in Germany?

The answer depends on the purchase price, your financing profile and the bank. Many expats should expect to bring significant equity. In practice, this can mean around 20 percent to 30 percent of the purchase price plus all "Kaufnebenkosten". For a property of 350,000 euros, this can quickly result in required equity of around 105,000 euros or more, depending on the mortgage structure.

What are property costs in Germany?

Property costs in Germany include one-time acquisition costs and ongoing running costs. One-time costs include "Grunderwerbsteuer", notary fees, land register fees and agent commission. Ongoing costs include "Hausgeld", property tax, maintenance reserves, insurance and possible special levies.

Do I need a mortgage before buying property in Germany?

You do not legally need a mortgage before searching for property, but in practice you should clarify financing early. Sellers and estate agents often take buyers more seriously when they already understand their home loan Germany budget and can show financing readiness.

Is Germany good for real estate investment?

Germany can be good for real estate investment if the buyer has a long-term perspective. Returns are usually not expected in the short term but rather through stability, rental demand and safe capital preservation. The German real estate market is generally better suited for conservative investors than for short-term speculation.

Is buying property in Germany worth it for expats?

Buying property in Germany can be worth it for expats who plan to stay long term, have stable financing and understand the full cost structure. It is usually less suitable for people who need maximum flexibility or expect quick short-term returns.

What should I check before buying property in Germany?

Before buying property in Germany, check the legal documents, purchase costs, mortgage approval, building condition, location, ongoing costs and long-term investment potential. These checks reduce the risk of legal, financial and structural surprises after purchase.

Which property documents should I check before buying in Germany?

Check the "Grundbuch" for ownership, charges, rights of use and restrictions. For apartments, obtain the "Teilungserklärung" and "Aufteilungsplan". Also check the "Hausgeld" statements, maintenance reserve, owners’ meeting minutes and any documents that show upcoming renovations or special levies.

Buying Property in Germany Without Costly Mistakes

Buying property in Germany should not be taken lightly. That is why we have put together this buying property in Germany guide to make things easier for you. The most important lesson is simple: do not focus only on the purchase price.

Understand the property documents, calculate all property costs Germany buyers face, check the mortgage structure carefully, and make sure the location fits your long term plan. If you prepare properly, buying property in Germany can be a stable and valuable long term decision.

If you have questions about buying a property in Germany or need expert help and advice, you can contact us for personal guidance. Our team of property and financing experts can help you understand your options before you commit to a purchase.