Most expats in Germany start in public health insurance. It feels safe, it is administratively simple, and it is widely accepted. You visit a doctor, the practice bills the insurer directly, and you rarely see invoices. For everyday life, that convenience is real.

But there is a second layer to the decision that many people overlook. Health insurance is not only a healthcare topic. It is also a financial planning topic. It affects your monthly cash flow, your ability to build reserves, and your long term resilience in Germany. As someone who advises expats on wealth planning and real estate decisions, I see a clear pattern. People treat health insurance as a background setting until the moment it becomes the most important decision in the room.

This article is not a blanket argument against public insurance, and it is not a promise that private insurance is always better. It is a practical explanation of why you should at least think about switching, especially if you plan to stay in Germany, build wealth, and want access to high quality care when it matters most.

Table of Contents

- How public and private health insurance work in Germany

- Why public health insurance is under structural pressure

- The hidden cost reality of public insurance

- Waiting times and access to specialists

- The two tier reality and self payer dynamics

- A real example where outcomes differ dramatically

- Martini Klinik results and why access matters

- Why this matters for wealth and real estate planning

- How to evaluate switching as an expat

- Next step and free orientation call

How public and private health insurance work in Germany

Germany has a dual health insurance system. Public health insurance is known as GKV. It is income based, and coverage is defined by law. Private health insurance is known as PKV. It is contract based, and the premium depends on factors such as age, health status, and the chosen tariff.

For many expats, the difference sounds simple. Public equals solidarity and simplicity. Private equals individual contracts and more options. What matters in practice is how these systems behave over time. Public insurance contributions follow income and system costs. Private insurance premiums follow medical costs, ageing, and the design quality of the tariff.

That is why the right question is not which system is good. The right question is which system fits your life plan in Germany, including family plans, income stability, and the level of medical access you want when a serious issue appears.

Why public health insurance is under structural pressure

Public health insurance in Germany is stable, but it is under structural pressure. People live longer and need more treatment. Medical innovation improves outcomes but increases costs. At the same time, the ratio of contributors to beneficiaries is shifting. Fewer working age contributors fund a larger group that requires more healthcare services.

This does not mean the system is failing. Germany will continue to deliver healthcare. But it does mean that the system has to manage rising demand with limited capacity. In practice, that pressure shows up in higher contribution rates, adjustments to reimbursement rules, and more friction in access to specialist care.

For expats, this matters because the decision you make today shapes the options you have later. If you assume public insurance will always provide the same experience, you may be surprised by gradual changes that become visible only when you need the system most.

The hidden cost reality of public insurance

Many people evaluate public insurance based on what is deducted from their salary. That is understandable, but incomplete. The real cost is often contributions plus the private payments people make to close gaps in access or quality.

In everyday life, this can show up as co payments, limited reimbursements in certain areas, and a growing market of services that are available quickly if you pay yourself. Public insurance is designed to provide a legally defined baseline. If your expectations exceed that baseline, you pay the difference.

That difference is not always dramatic, but it accumulates. Over years, repeated out of pocket payments can become meaningful. More importantly, they can create a situation where you pay a high monthly contribution and still cannot reliably access the level of speed or specialization you want.

Private health insurance does not remove all costs and it does not guarantee a perfect experience. But it can shift the structure. With the right tariff, you are buying a contract that targets access and medical options more directly, rather than relying on the capacity constraints of a large public system.

Waiting times and access to specialists

Waiting times are one of the most visible differences between public and private insurance. In many regions and specialities, public patients wait weeks or months for specialist appointments. When the issue is minor, this feels like inconvenience. When the issue is urgent, waiting becomes stress, uncertainty, and a real risk factor.

In my client work, I often see a practical workaround. Public patients pay privately for diagnostics, specialist consultations, or faster appointments. The system works, but it creates a hidden two step process. First you are insured publicly. Then you pay privately anyway when speed matters.

From a financial planning perspective, time is not only comfort. Time is risk. Delayed diagnostics can lead to delayed treatment. Delayed treatment can lead to longer recovery, missed work, and higher indirect costs. Even when the final medical outcome is fine, the stress cost is real and often underestimated.

Private health insurance can improve access by allowing more flexibility in provider choice and appointment scheduling. It cannot promise outcomes, but it can improve the probability of being seen sooner and by more specialized teams.

The two tier reality and self payer dynamics

Many expats arrive in Germany expecting a uniform healthcare experience. In practice, a two tier reality exists in many settings. Practices and hospitals operate with different reimbursement structures. Private patients can be prioritized, and self payer options are often available to public patients who can afford them.

This is not a moral judgement about doctors or clinics. It is a market response to capacity and incentives. When demand exceeds supply, access becomes differentiated. That differentiation can be based on insurance status or on the ability to pay privately.

The question is not whether this exists. The question is how you want to navigate it. Some people accept the public system and pay privately when needed. Others prefer a contract structure that increases access and reduces the need for repeated private payments.

A real example where outcomes differ dramatically

There are situations where the difference between average care and highly specialized care is not a small detail. It can shape quality of life for years.

Prostate cancer is one of the most common cancers among men. A widely cited lifetime risk is roughly one in seven men. The diagnosis is frightening, but many patients fear the potential side effects of treatment just as much as the disease itself.

Two of the most common long term side effects after prostate cancer surgery are incontinence and erectile dysfunction. The reality can be tough. Many men experience some level of urinary leakage after treatment, and erectile function can be significantly affected.

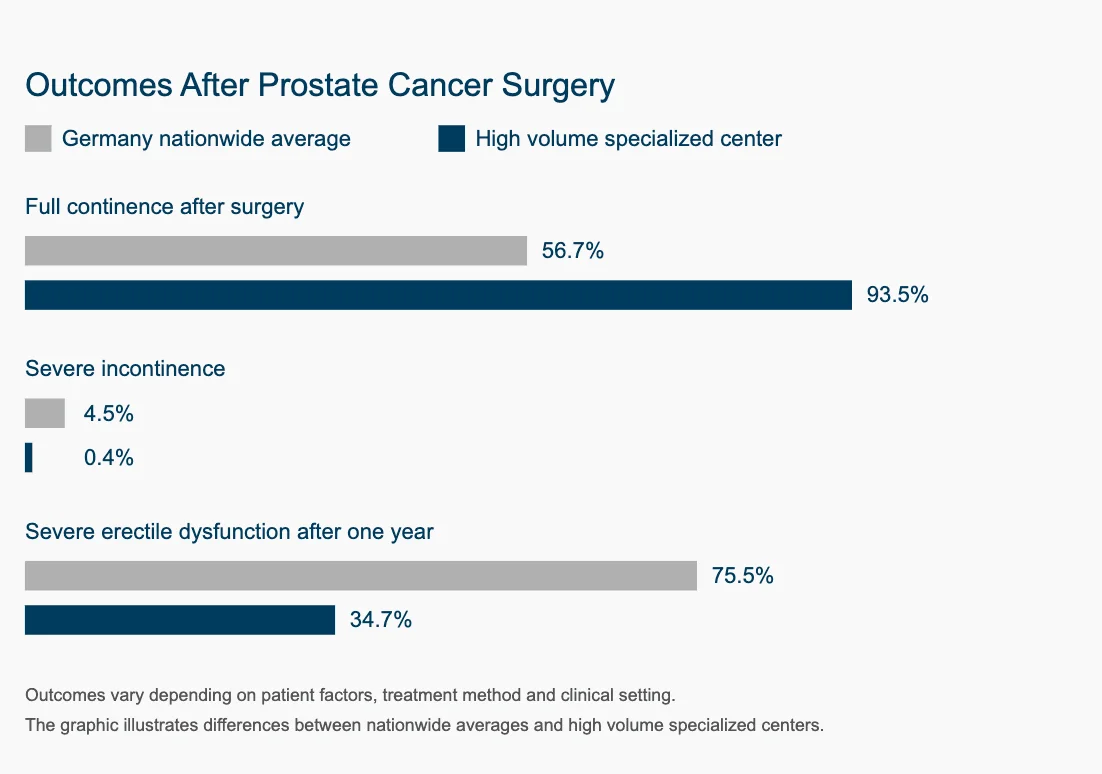

What many people do not realize is how strongly outcomes can vary between centers. Modern nerve sparing surgery and robotic methods can reduce complications, but the most important factor is often experience. Surgeons and teams who perform a high number of procedures per year tend to achieve better functional outcomes because precision improves with volume, process, and specialization.

In practical terms, a high volume specialized center can reduce the risk of severe incontinence into the low single digits in some reporting, and it can meaningfully reduce the rate of severe erectile dysfunction after one year compared to broader averages. No clinic can guarantee results, and individual outcomes depend on patient factors, disease stage, and treatment details. But the difference in probability matters.

Martini Klinik results and why access matters

A well known example of a high volume specialized center in Germany is Martini Klinik in Hamburg, which publishes outcome reporting. Their reported figures are often referenced in discussions about how surgical volume and specialization can influence continence and erectile function outcomes after prostate cancer surgery.

For transparency, you can review their published results here: https://www.martini-klinik.de/klinik/resultate.

The insurance relevance is straightforward. Access to specific centers can depend on insurance pathways, additional coverage, or self payer decisions. The difference is not that private insurance guarantees the best clinic for every situation. The difference is that private insurance can increase access and flexibility when choosing specialized providers and treatment pathways.

This is the point many expats miss. Private health insurance cannot promise perfection. But it can give you a better chance of getting the best possible option available within the system. In high impact situations, that probability is worth discussing seriously.

Why this matters for wealth and real estate planning

At first glance, health insurance and real estate planning may seem unrelated. In reality, they are connected through cash flow and risk planning. Monthly insurance costs affect how much you can save, invest, and allocate to housing. Unexpected medical related payments affect reserves. And financial stability affects how confidently you can commit to a mortgage and long term property ownership in Germany.

If you are exploring property markets, you can use the Real Estate Search Engine to compare locations and opportunities based on your personal criteria: Real Estate Search Engine.

Once you have a property scenario, it helps to stress test your numbers. Many people underestimate how a few hundred euros difference in monthly costs changes long term affordability and investment returns. The Property Investment Calculator is designed to model exactly these kinds of scenarios: Property Investment Calculator.

The main idea is simple. Health insurance is not a side topic when you plan to build wealth in Germany. It is part of the foundation that supports long term stability.

How to evaluate switching as an expat

Switching to private health insurance should not be rushed. It requires an honest assessment of your situation and your priorities. Income stability matters. Family planning matters. Risk tolerance matters. Administrative comfort matters, because private insurance typically involves invoice handling and reimbursement processes.

Public insurance remains a strong choice for many families, especially where one partner does not work or where multiple children are planned. Private insurance can be a strong choice for others, especially where income is high and stable, and where access, flexibility, and specialized care are priorities.

The mistake is not choosing one system over the other. The mistake is choosing based on a short term headline such as cheaper today, without understanding the long term consequences and the access dynamics that become relevant under pressure.

Next step and free orientation call

If you want clarity on whether private health insurance makes sense for your situation, the most effective next step is a short orientation call. The goal is not to push a switch. The goal is to map your personal scenario, identify risks, and avoid costly mistakes.

You can book a free consultation with FFE here: https://financeforexpats.de/contact.

If you want more detail, personalized advice, or help aligning insurance choices with your long term wealth and real estate plan in Germany, reaching out to FFE is the right step.