Buying property in Germany is a major commitment and the purchase is only the beginning. You spend months finding the right place, negotiating the deal, and signing the contracts. Then the keys arrive and it feels like the hard part is over. It is not. Property insurance in Germany is what protects everything you have just built if life does not go to plan.

Understanding property insurance Germany is essential for expats looking to protect their property and build long term wealth.

Whether you are navigating the Grundbuch for the first time or already own property here, this guide walks you through exactly what you need, what it costs, and when you need to act.

Property Insurance Germany Navigation and Structure

The German insurance landscape is comprehensive, sometimes overwhelmingly so for newcomers. To make property insurance Germany manageable, we have structured this guide into three actionable steps:

- Step 1: The universal insurance foundation applies to everyone, regardless of property type

- Step 2: Property type and life situation variables where your specific circumstances start to matter

- Step 3: Your action plan, deadlines, costs, and exactly what to do next

Step 1: The Universal Foundation of Property Insurance Germany

Whether you rent or own, these three types of insurance in Germany are your non negotiable baseline. They apply to every expat, every homeowner, every tenant. Budget for them first. Everything else builds on top.

Personal Liability Insurance in Germany (Haftpflichtversicherung)

This one surprises most people coming from other countries. Personal liability insurance in Germany is unique because German law makes liability unlimited. There is no cap. If you accidentally flood the flat below you, knock over someone else's expensive camera, or cause a cycling accident, you are personally responsible for every euro of the cost.

At EUR 5 to EUR 10 a month, this is the most important and most overlooked piece of expat insurance Germany newcomers miss.

- Cost: EUR 5 to EUR 10 per month

- Covers: Damages you cause to others or their property

- Tip: Look for Forderungsausfalldeckung. It protects you when someone causes you damage but has no insurance to pay.

Household Insurance Germany: Contents Insurance Explained

Household insurance Germany (Hausratversicherung), also known as home contents insurance or household contents insurance, covers everything inside your home. It is the household contents insurance equivalent of renters insurance Germany or tenant insurance you may know from elsewhere. Furniture, electronics, and clothes are all protected against theft, fire, water damage, and vandalism.

- Cost: EUR 6 to EUR 18 per month

- Covers: All personal belongings inside your home

Legal Protection Insurance in Germany

Disputes with landlords, neighbours, or employers are expensive in Germany. Legal protection insurance covers attorney fees and court costs, an essential part of any home and household insurance strategy.

- Cost: EUR 27 to EUR 38 per month

Universal Insurance Cost Baseline in Germany

Your total property insurance Germany baseline is EUR 39 to EUR 69 per month. This applies to everyone, renters and owners alike. All cost tables in Part 3 show additional costs only. Always add this baseline to your total.

Property Insurance Germany: Part 2 Property Specific Variables

Once the foundation is covered, home insurance Germany and house insurance Germany requirements diverge based on what you own and how you use it.

Home Insurance Germany: Property Type Differences

Apartment (Owner Occupied): Building insurance is typically handled by the homeowners association (WEG). Focus on liability and household contents.

House (Owner Occupied): You carry full structural responsibility. House insurance Germany (Wohngebaeudeversicherung), also known as building insurance (Gebaeudeversicherung), is mandatory for mortgage approval and must include elemental damage coverage.

- Cost: EUR 45 to EUR 120 per month

- Must include: Flood, storm, and elemental damage protection

Property Insurance Germany: One Month Decision Window After Purchase

One of the most time sensitive moments in property insurance Germany is the day your name appears in the Grundbuch. From that date, you have 30 days to keep the previous owner's building insurance or switch to a new policy. Miss this window and the choice is locked.

Action required: Contact us the moment your Grundbuch notification arrives. As independent brokers, we analyse both options and advise you either way. Use our Real Estate Search Engine if you are still searching for the right property.

Insurance in Germany Based on Property Usage

Owner Occupied: Focus on income protection and mortgage security.

Rental Property - Landlord Insurance Germany: Additional requirements:

- Landlord Legal Protection: EUR 11 per month

- Rent Default Insurance (Mietausfallversicherung): EUR 50 to EUR 83 per month. Pays your rent directly when tenants stop paying.

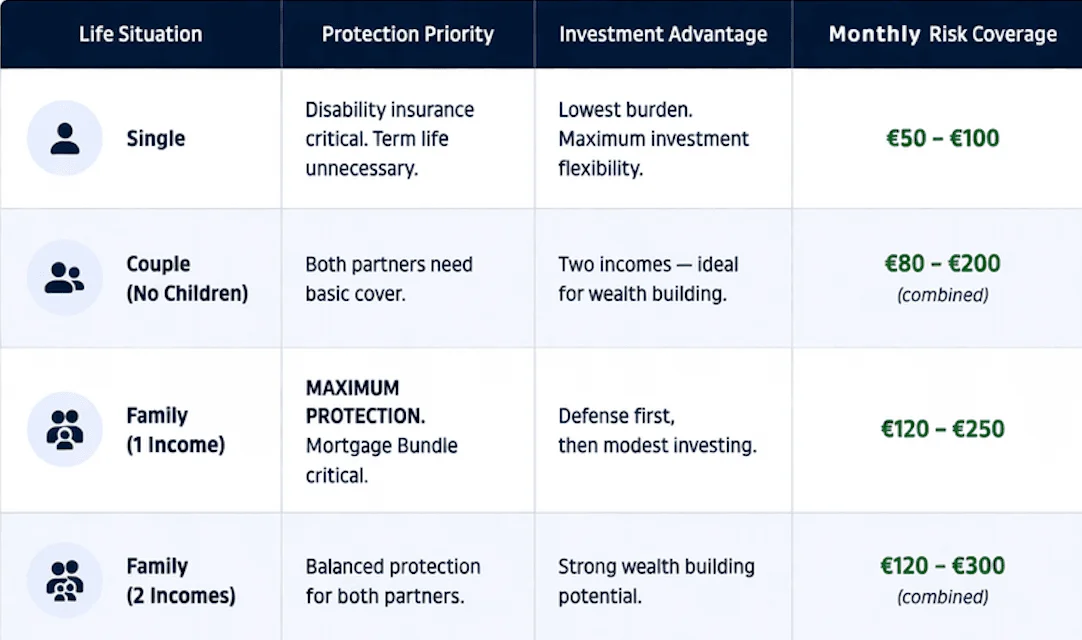

Part 3 Risk Protection Strategy in Germany by Life Situation

The right insurance in Germany setup depends on your life, not just your property. This is especially relevant for expat insurance Germany clients building financial stability in a new country.

Insurance Strategy Overview by Life Situation

The following overview shows how property insurance Germany strategies differ depending on your life situation. Costs below cover existential risk only. Add Part 1 baseline and building insurance where applicable.

Insurance Strategy for Singles in Germany

No dependents means no term life needed. Your entire insurance in Germany focus goes toward protecting your income. If you cannot work, there is no second salary to cover the mortgage, so occupational disability (Berufsunfaehigkeitsversicherung) is your most critical policy. The upside is a low insurance burden, which means more cash flow to invest, making this the best position for expat insurance Germany wealth building.

Insurance Strategy for Couples Without Children

Two incomes and no dependents is one of the best financial positions you can be in. Keep home and household insurance lean, cover each other at modest sums, and direct the surplus into building real wealth. If one partner faces a short term setback, the other can usually hold things together, which means you can afford to take slightly more risk with your investments.

Insurance Strategy for Families with One Income

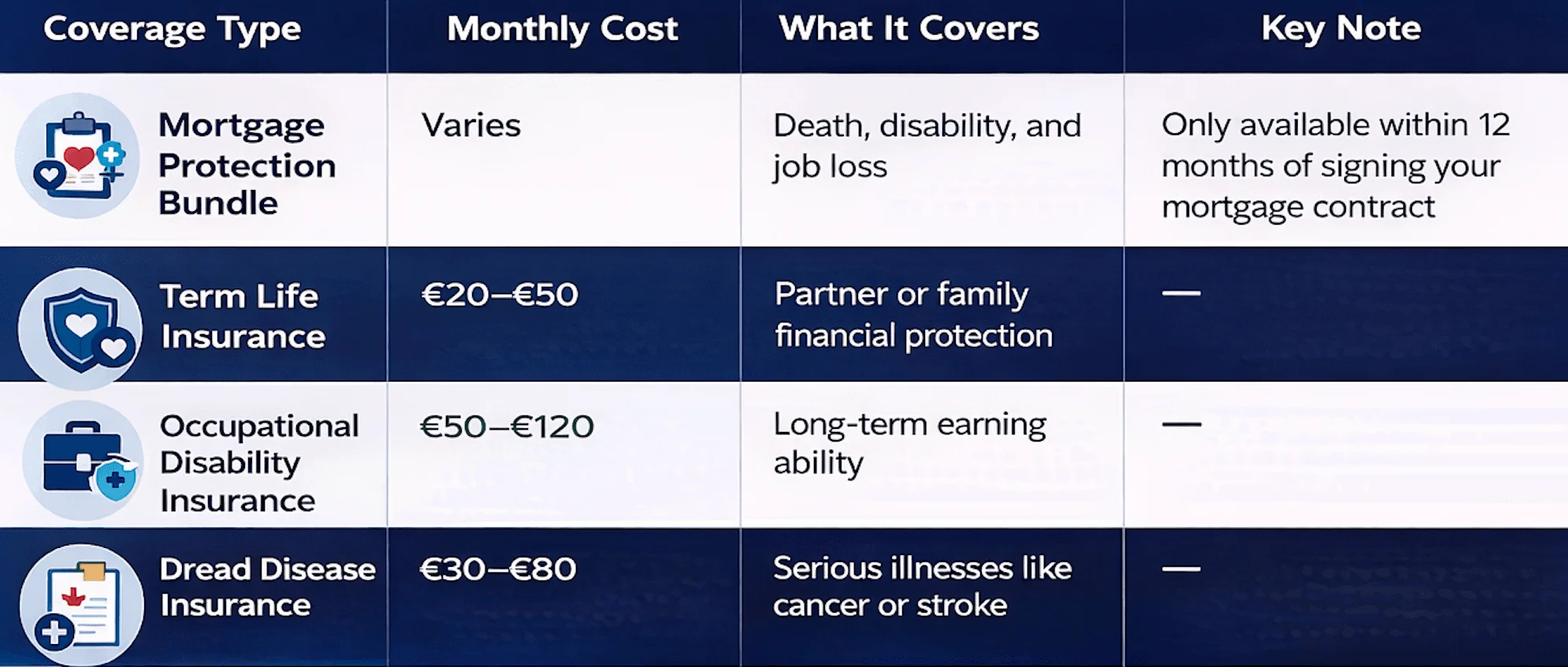

This is the highest risk scenario in property insurance Germany planning. One income, one mortgage, zero backup. If the primary earner cannot work, the entire financial structure, including the home, is at risk. The mortgage protection bundle is non negotiable. Build the emergency fund before you invest a single euro elsewhere. Defense comes first.

Insurance Strategy for Families with Two Incomes

More flexibility, better balance. Both partners need coverage, but one income can temporarily support the household if needed. A practical approach: one partner's surplus builds the emergency fund while the other invests. This gives you both protection and growth within your overall property insurance Germany strategy.

Key Risk Protection Components in Germany

Part 4 Property Insurance Germany Wealth Strategy Beyond Protection (The Gold Savings Plan Strategy)

Good property insurance Germany protects what you have built. But protection alone does not grow wealth. Once your coverage is in place, what you do with the remaining cash flow matters just as much.

Traditional Mortgage Repayment Strategy

Most homeowners follow the same instinct: funnel extra cash into mortgage overpayments. It feels responsible, it reduces debt, and it saves interest. But there is a real cost that rarely gets mentioned. It permanently locks your liquidity. Every extra payment you make disappears into the wall. You cannot get it back in an emergency, and you are earning a return equal to your mortgage rate, typically 3 to 4 percent, when that money could potentially be working much harder.

Wealth Building Strategy Through Investment

What forward thinking expat insurance Germany clients are doing instead: keep the mortgage at its contractual minimum and systematically invest the surplus into a gold savings plan. The money stays liquid and accessible. Returns have historically outpaced German mortgage rates over 10 to 15 year periods.

Why This Strategy Outperforms in Germany

- Liquidity: Gold stays accessible. Extra mortgage payments do not.

- Returns: Mortgage rates run 3 to 4 percent. Gold has historically outperformed over 10 to 15 year periods.

- Payoff power: Build a wealth pool, then use it to wipe out large chunks of your mortgage in one move.

- Diversification: Your net worth spans property and precious metals, not just bricks.

Use our Property Investment Calculator to see how this changes your 15 year net worth.

Part 5 Critical Insurance Reminders in Germany for Expats

Health Impact on Insurance Costs in Germany

Your health is your currency when it comes to insurance in Germany. Diabetes can make disability cover nearly impossible to obtain and doubles term life premiums. Any pre existing condition typically triggers a 50 to 100 percent surcharge, or outright denial. For expat insurance Germany planning, the message is simple: secure your coverage while you are healthy. This is the one deadline nobody sends you a reminder about, and it gets more expensive with every month you wait.

Important Insurance Deadlines in Germany

- Mortgage Protection Bundle: Must be signed within 12 months of your mortgage contract.

- Grundbuch window: 30 days to change building insurance in Germany after property transfer.

Cost Saving Strategies for Insurance in Germany

Pay household insurance Germany and other policies annually. Most providers offer 1 to 5 percent off versus monthly billing. Small per policy, meaningful across several.

Property Insurance Germany Action Plan for Expats (3 Step Action Plan)

Immediate Action Step (This Week)

Book a consultation and get baseline coverage in place. If you bought property in the last 30 days, contact us before anything else. The Grundbuch window may already be closing.

Book your free consultation here

Total Monthly Property Insurance Cost Overview

Property Insurance Germany Cost Breakdown Diagram

Layer it up: baseline first, then building insurance if you own a house, then risk protection matched to your life situation, then wealth building investment on top. Together, these form a complete home insurance Germany and household insurance Germany strategy, not just a list of policies.

FAQs About Property Insurance Germany

What is property insurance in Germany?

A combination of Gebaeudeversicherung (building) and Hausratversicherung (contents), covering the structure and everything inside it.

Is household insurance mandatory in Germany?

Not legally, but landlords and mortgage lenders typically expect it, and skipping it rarely pays off.

What does household insurance cover?

Furniture, electronics, and clothing against theft, fire, water damage, and vandalism.

Do expats need insurance in Germany?

Yes, especially liability. German law makes liability unlimited, so one accident without cover can be catastrophic. Expat insurance Germany should always start here.

How much does property insurance cost in Germany?

Baseline is EUR 39 to EUR 69 per month. Home insurance Germany for house owners adds EUR 45 to EUR 120. Risk protection varies by life situation.

Final Thoughts on Property Insurance in Germany

Good property insurance Germany is not about buying every policy available. It is about understanding where your real risks are, covering them systematically, and making sure your protection decisions leave room for your financial life to actually grow.

The people who get this right, especially expat insurance Germany clients who arrive with no prior knowledge of the system, tend to share one trait: they act early. They secure coverage while healthy. They do not miss the Grundbuch window. They build the baseline before layering anything else on top. Start there, match everything to your actual life situation, and the rest follows.