Buying property in Germany as an expat and getting approved for a mortgage is absolutely possible if you are well prepared. Most German banks are very conservative and require a lot of documentation. As soon as there is a small mismatch in your financial history, your mortgage application may be declined. With this guide, expats will know what they can expect from German banks and how to increase their chances of mortgage approval in Germany.

This is a complete guide to mortgage in Germany for expats and international buyers. It includes the key things you need to know before you apply for a home loan in Germany. We explain in detail how a mortgage in Germany works, what German banks are looking for in a potential buyer, and the most common reasons for mortgage applications to be rejected. Most importantly, we also explain what you can do to improve your chances of mortgage approval in Germany.

Why Getting a Mortgage in Germany Is Different for Expats

Buying property in Germany as an expat and getting a home loan is possible, but rejection is often more likely than many people expect if the application is not properly prepared.

The German mortgage system runs on the basis of very conservative lending models. German banks therefore want to be close to 100 percent sure that their clients are able to repay their debts on time before they actually grant them a loan. The conservative business policy of German banks means that it is often harder to get a mortgage approved than in other countries like the US or UK. For expats however, there are a number of potential issues when trying to obtain a mortgage in Germany.

For example, expats will typically not have a sufficient credit history with the German credit reference agency SCHUFA, they may have temporary contracts of employment, and they may receive income from abroad. You are not alone, as the mortgage application process for expats is well known to fail for the reasons outlined above. That does not mean you cannot get a home loan in Germany, it simply means you should be well prepared before you start the application process.

If you want support with your specific mortgage application, documentation, or financing structure, you can also reach out through our contact page.

How a Mortgage in Germany Works

Mortgages in Germany are typically long term loans secured against a property in Germany. That property is often bought at the same time as the mortgage is agreed. The mortgage is then repaid by the borrower over a period of 15 to 30 years. In terms of structure, a large number of German mortgages are fixed for a number of years, known as the "Zinsbindung". For example, 5 years, 10 years or 15 years.

During this fixed period, the borrower repays a fixed amount every month. This amount remains the same for the agreed period and includes both interest and part of the principal amount of the mortgage. Once the fixed period comes to an end, the interest rate can be refinanced on the basis of the then current interest rates on the market. This is why the point at which a mortgage is agreed is so important. After fixing the interest rate for 5 to 15 years, the loan can later be refinanced at new market interest rates. This is why it is very important to arrange your home loan at the right time on the market in order to obtain the lowest interest rate possible for the longest possible fixed interest rate period.

Mortgage Interest Rates in Germany

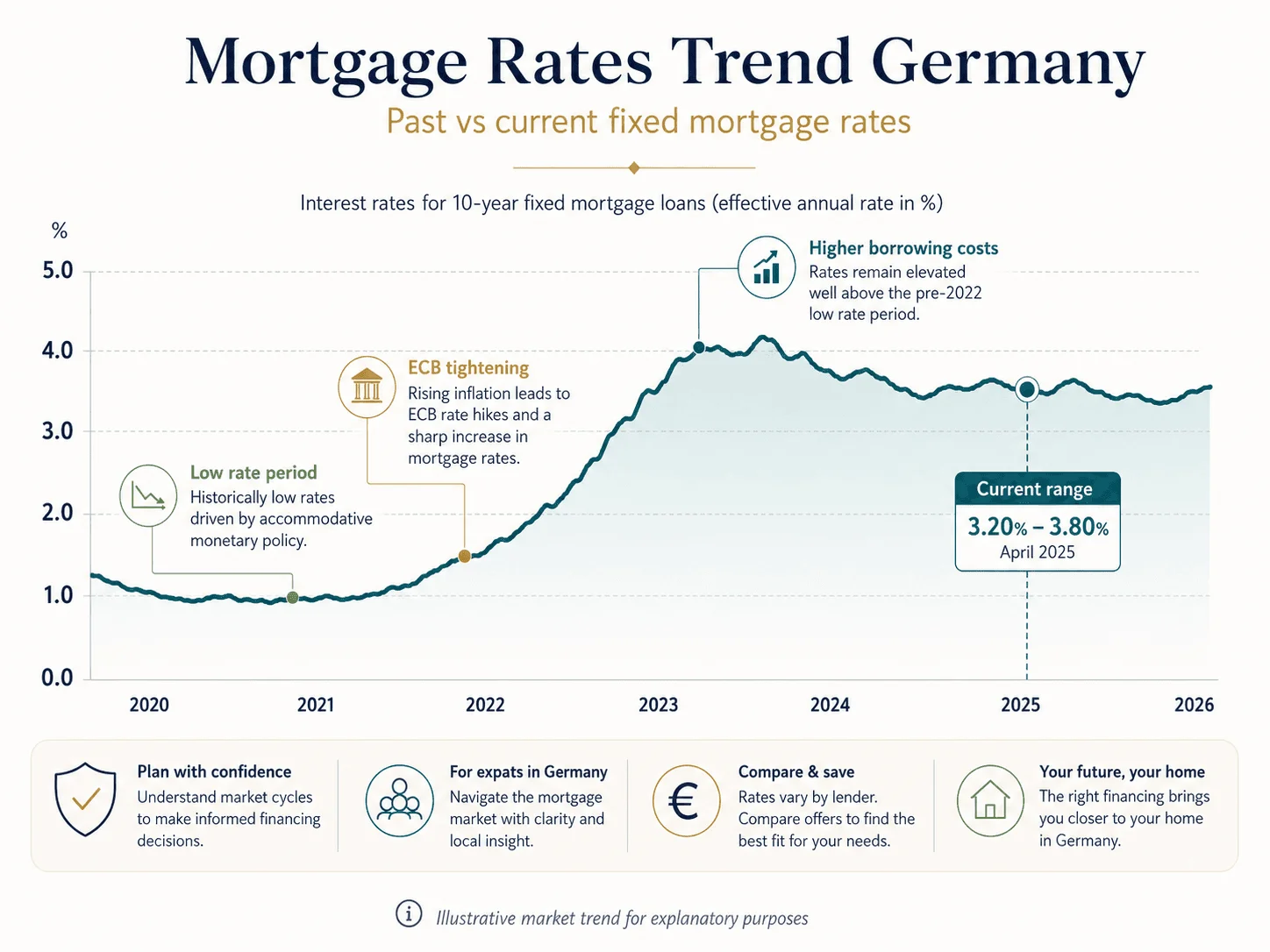

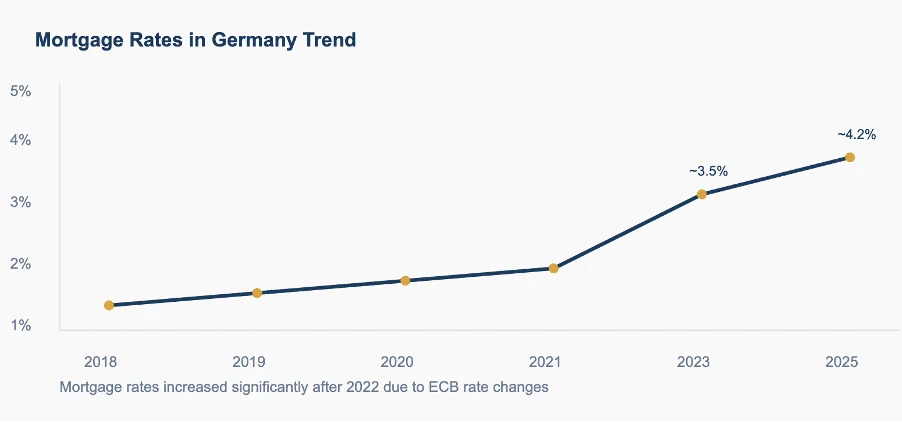

Mortgage interest rates in Germany are influenced by the base rate of the European Central Bank (ECB) , the so called refinancing rate. In general, if the ECB cuts the base rate, borrowing in Germany tends to become cheaper. On the other hand, if the ECB increases the base rate, borrowing in Germany becomes more expensive. Due to current developments on the European financial markets, mortgage interest rates in Germany have increased significantly compared with the very low levels seen in the past.

For example, for a fixed rate mortgage of 10 years, mortgage rates in Germany can vary considerably depending on the bank, the borrower profile and the market environment. This means that a difference of just 1 percent can lead to additional costs in the region of tens of thousands of euros over a 20 year repayment period. The interest rate fixed at the time of the mortgage application thus plays a very important role for the expatriate. There are also variable interest rates, but in contrast to some other countries, variable interest rates on mortgages are not as common in Germany. The reason for this is quite simple: with a fixed interest rate for a mortgage in Germany, the borrower knows exactly how much interest has to be paid every month for the fixed interest period. This makes financial planning much easier.

This mortgage rates trend chart helps illustrate why timing matters so much when comparing current mortgage rates in Germany and longer term affordability.

Deposit and Loan to Value in Germany

Many banks require a minimum down payment of 10 percent to 20 percent of the purchase price. However, for expats the minimum can be even higher. Therefore it is recommended to bring more than the required minimum down payment in order to improve approval chances and obtain the best possible mortgage interest rate.

An additional important factor for mortgage applications of expats is their loan to value ratio, in other words the proportion of the purchase price of a property which a bank is willing to lend to you.

Generally speaking, the lower the loan to value (LTV) ratio, the better your chances for mortgage approval as well as a favourable interest rate. For non resident expats, bringing a large down payment to a property purchase in Germany is typically the best way to get approved for a home loan. In order to get a mortgage loan in Germany as an expat or non resident, you will in most cases have to finance 30 percent up to 40 percent of the purchase price yourself as a down payment. Many German banks grant mortgage loans to expats and non residents at a loan to value ratio of 60 percent up to 70 percent. In this case the bank takes on less risk and therefore also grants a more favourable interest rate for the mortgage.

Mortgage Approval Process in Germany

Property financing in Germany is often a lengthy process because the bank needs to assess the risk it takes when granting mortgage approval. As a guide, the following steps are typically taken to process the financing of a property:

- Initial consultation with a bank or mortgage broker

- Submission of documents such as income, employment and property details

- Bank performs credit and risk assessment

- Conditional approval or request for further documentation

- Property valuation by the bank

- Final approval and signing of the loan agreement

The process to receive a mortgage can take time and can be stressful. Typically, you should count on several weeks. Usually, delays are due to missing documentation. But if you are already well prepared before you start your mortgage search, this should not become a major issue.

This mortgage approval process diagram gives expats a quick overview of the typical steps from first consultation to final loan approval.

What German Banks Check Before Mortgage Approval

German banks review your complete financial situation in full detail. The most important mortgage requirements in Germany for them are:

- Sufficient and stable income from all sources in relation to the amount of the agreed mortgage

- The borrower's employment status, whether permanent or temporary, or whether he or she is self employed

- SCHUFA score and overall credit history within Germany

- Deposit amount and any additional financial reserves

- Existing loans and liabilities of the applicant which reduce the maximum amount of money that the bank is willing to grant

- Your overall risk profile as a borrower

Why Mortgage Applications Get Rejected in Germany

More expats in Germany than expected recently have their mortgage applications rejected by German banks. Below you can find the typical reasons for mortgage rejection for both German citizens and expats abroad:

- Probation period or fixed term contract

- Low or absent SCHUFA score

- Insufficient deposit or a high loan to value ratio

- High debt to income ratio

- If the applicant or co applicant earns money from self employment or freelance work without stable and properly documented income history, this can be a problem for the application

- The bank considers the property too risky and fears that its value may drop

It is generally wise to refrain from submitting a mortgage application if you are on probation, newly arrived in Germany, or already carrying a lot of debt. If a bank rejects a mortgage application, this may also be recorded on your credit file.

Mortgage Rates and Affordability in Germany

The current mortgage interest rates on the German market have a huge impact on how much mortgage you can afford to pay back in order to service the interest on the mortgage. As a rule of thumb, German banks often say that around 30 percent to 35 percent of your monthly net income should be used to cover the monthly repayments on the mortgage.

Here is an example of a mortgage with a loan of € 300,000, a fixed interest rate and a term of 10 or 20 years:

| Loan Amount | Interest Rate | Monthly Payment Approx. |

|---|---|---|

| €300,000 | 3.5% | ~€1,500 |

| €300,000 | 4.5% | ~€1,650 |

| €300,000 | 5.5% | ~€1,800 |

An increase of 1 percent in interest could add another €150 to your monthly repayment costs. When translated into interest payments over a 30 year period this can amount to no less than €54,000. It is thus essential that you first and foremost get an idea of the costs of the mortgage in relation to your financial resources before you start your property search. Use a mortgage calculator Germany to calculate the costs of the various financing options.

If you also want to compare repayments, ownership costs and longer term returns more realistically, the Property Investment Calculator is a useful next step.

How Expats Can Improve Their Mortgage Approval Chances

Applying for a mortgage as an expat can be a challenging and time consuming process. In order to be properly prepared, we have put together a list of the most relevant factors which will positively affect your mortgage application.

Mortgage approvals in Germany are often strengthened by more equity. The more deposit you bring, the lower the risk for the bank. So 20 percent or more of the purchase price would be ideal.

Being on a permanent contract with your employer is in most cases the single largest factor when it comes to getting a mortgage approved. Until your permanent contract has started, it is often better to wait a bit rather than risking a refusal due to your current employment status.

Build your SCHUFA credit history. Open a bank account, apply for a credit card and make your payments on time for your existing contracts. It takes time to build up a good credit history but it is worth starting as soon as you arrive in Germany.

Reduce your debts. Before even starting your mortgage search it is a good idea to pay down outstanding loans and credit and to clear your credit card balances. The bank will look on these as liabilities and they will affect your creditworthiness.

Organize all documents required for a mortgage application in due time. In addition to salary statements, German mortgage banks such as HypoBank or LBBW require among other things your tax returns from previous years, your employment contract, your bank account statements as well as the technical documents of the building to be financed.

Whether you need help selecting the proper mortgage or need assistance getting approved by a bank that provides mortgages to expats, a mortgage broker who is familiar with the requirements for expats as well as the German mortgage market in general is often a very good place to start.

Costs of a Mortgage in Germany

A mortgage in Germany does not only consist of interest rates. Other costs, such as bank charges and insurance, have to be considered before signing a contract. Repayment costs on the mortgage over the entire term of the contract are the biggest single long term cost on your new home. To keep these costs as low as possible, it is essential to get the lowest possible interest rate on your new mortgage from the start. In addition to the interest rate on your loan, as a homeowner in Germany you will also have to pay the usual bank charges, as well as premiums on building insurance (Wohngebäudeversicherung).

One off purchase costs of a property in Germany are often underestimated by expats. The most important are:

- Grunderwerbsteuer or property transfer tax: 3.5 percent to 6.5 percent of the purchase price depending on the federal state

- Notarkosten or notary fees: approximately 1.5 percent to 2 percent

- Maklerprovision or estate agent commission: up to 3.57 percent per party

These costs need to be covered by the buyer from their own funds and are therefore not financed by the mortgage. These so called purchase costs amount to around 10 percent to 15 percent of the purchase price. That is why mortgage costs in Germany should always be calculated together with purchase costs and ownership costs, not just the interest rate.

To model these costs more clearly before buying, use the Property Investment Calculator.

Choosing the Right Property for Mortgage Approval

The property itself also plays a role in mortgage approval. German banks look at the location of the property, the demand on the local property market and the long term value of the property. The bank also assesses the property that is to be financed with the mortgage.

This can be divided into several criteria.

Firstly, the bank is interested in the location of the property. City centres in large cities such as Berlin, Munich and Frankfurt are generally viewed more positively than locations in the outlying areas of towns and villages. In terms of demand, banks assess the number of buyers who are interested in the type of property that is to be financed.

In addition to these two criteria, banks also try to assess the long term value of a property on the market. A property with a large garden in the countryside may have a lower long term value in the eyes of the bank, therefore it may be more difficult to get a mortgage approved for such a property. It is therefore very important to select a property which the bank views as having a high long term value on the market.

Most importantly, banks are interested in the location of the property, its demand on the market as well as its future value. If the banks perceive a property to be a good, liquid asset in the long term, they are more likely to grant a mortgage for this property than for one that is perceived to have a lower value in the future. In such cases, the banks may approve the mortgage but with very strict conditions.

If you want to compare properties that are more likely to match lender expectations in terms of location and market demand, the Real Estate Search Engine is a useful tool.

Common Mortgage Mistakes Expats Make

Mortgage applications of even well prepared expats fail for various reasons. But many of these mistakes can be avoided.

One of the most common mistakes is underestimating the total cost of ownership. This is even more common than underestimating the costs of buying a property in the first place, including purchase costs, mortgage repayment, maintenance, insurance and other long term obligations.

Another mistake is not understanding the specific structure of a mortgage, for example fixed rate loans that are then refinanced after a specific term with then current market interest rates. It can be very expensive to refinance at the wrong time.

Applying for a mortgage too early is another common error. Many expats start their mortgage search as soon as they have found a property and begin applying for mortgages before they have secured a permanent contract, before their SCHUFA records have started to show a positive trend, or before they have managed to save a sufficient deposit.

In many cases, banks will reject such applications immediately.

Ignoring interest rate risk is also a major issue. Many mortgage borrowers in Germany agree on a fixed interest rate for a short period of time, for example 2 years, with the hope of locking in a relatively low rate. However, until the fixed rate period has come to an end, there is always a risk that interest rates on the market will rise significantly in the meantime. This can be very unfavourable for the borrower when the fixed rate period comes to an end.

Finally, many expats fail to compare mortgage offers from different banks. One bank may decline a mortgage application while another bank will approve the same application on different terms.

Frequently Asked Questions About Mortgages in Germany

Can expats get a mortgage in Germany?

Even foreign residents can get a mortgage in Germany to buy a home. However, every application is checked on a case by case basis. The criteria are based on several factors including how stable the borrower's income is, the nature of their employment, their SCHUFA rating and their deposit.

How much deposit is required in Germany?

The amount of deposit required by Germans and expats alike is usually between 10 percent and 20 percent of the purchase price of a property. However, as the risk for the bank is often higher for expats, they may be required to put down a larger deposit.

What are current mortgage rates in Germany?

Current mortgage interest rates vary over time depending on the market and the borrower profile. When you compare offers from various mortgage providers that have accepted your expat mortgage application, you should use a Germany mortgage calculator to compare their offers on a repayment basis.

Is a permanent contract required for a mortgage?

A permanent employment contract is not an absolute legal requirement in every single case, but in most cases it significantly improves approval chances and is expected by many lenders.

How long does mortgage approval take?

Mortgage approval can take anywhere from around 3 weeks to 3 months. This depends on how fast all required documents are put together completely and how quickly a bank processes the application.

Getting a Mortgage in Germany as an Expat

A mortgage in Germany is achievable, but it rewards preparation. Understanding how home loans in Germany are structured, what banks look for, and where applications typically fall apart puts you in a much stronger position than going in blind.

Start building your financial profile early. Understand the true costs involved. Choose your property wisely. And do not rush the process. A well timed, well prepared application will always outperform a hasty one.

If you want guidance specific to your situation, get in touch through our contact page. The German property market is navigable, you just need to know the rules.